Debt Consolidation Loans with No Origination Fees Our Top Picks

Find the best debt consolidation loans that come with no origination fees helping you save on upfront costs.

Find the best debt consolidation loans that come with no origination fees helping you save on upfront costs.

Debt Consolidation Loans with No Origination Fees Our Top Picks

When you're looking to consolidate debt, every penny counts. Origination fees, which are charges some lenders impose for processing your loan application, can eat into your savings and make your debt consolidation less effective. These fees typically range from 1% to 8% of the loan amount, and while they might seem small, they can add up significantly, especially on larger loans. Imagine taking out a $20,000 debt consolidation loan with a 5% origination fee – that's $1,000 you're paying just to get the loan, money that could have gone directly towards reducing your principal. That's why finding debt consolidation loans with no origination fees is a smart move for anyone looking to streamline their finances and maximize their savings.

This guide will walk you through why no-origination-fee loans are beneficial, what to look for, and our top picks for lenders offering these cost-saving options. We'll also delve into specific product comparisons, use cases, and even some pricing insights to help you make the most informed decision for your financial future.

Understanding Origination Fees and Their Impact on Debt Consolidation

Let's break down what an origination fee actually is. It's essentially an administrative charge from the lender for setting up your loan. Think of it as a processing fee. While some lenders use it to cover their costs, others see it as an additional revenue stream. The key takeaway here is that it's an upfront cost. This means that if you borrow $10,000 with a 3% origination fee, you'll only receive $9,700, but you'll still be paying interest on the full $10,000. This effectively increases your Annual Percentage Rate (APR) and reduces the actual amount of debt you can consolidate with the same loan amount. For someone trying to get out of debt, every dollar matters, and avoiding these fees can significantly impact your overall savings and the speed at which you become debt-free.

The impact of origination fees can be particularly pronounced for those with less-than-perfect credit. Lenders often charge higher origination fees to borrowers they perceive as higher risk. This creates a double whammy: you might already be facing higher interest rates, and then you're hit with a substantial upfront fee. This is why actively seeking out lenders who offer no-origination-fee debt consolidation loans is a crucial step in optimizing your debt relief strategy.

Benefits of Choosing Debt Consolidation Loans Without Origination Fees

The advantages of opting for a debt consolidation loan without an origination fee are clear and compelling. First and foremost, you save money. This might seem obvious, but the direct financial benefit is substantial. Every dollar not spent on an origination fee is a dollar that can go towards paying down your principal, reducing your interest accrual, and ultimately shortening your debt repayment timeline. This direct saving can translate into hundreds or even thousands of dollars over the life of the loan.

Secondly, it simplifies your financial planning. When you don't have to factor in an upfront fee, the amount you borrow is the amount you receive, making it easier to calculate exactly how much debt you can consolidate and what your true monthly payments will be. This transparency is invaluable when you're trying to get a clear picture of your financial situation.

Thirdly, it can lead to a lower effective APR. As mentioned earlier, an origination fee effectively increases the cost of borrowing. By eliminating this fee, the stated interest rate on your loan is a more accurate reflection of your true borrowing cost, making it easier to compare offers from different lenders. This can be a game-changer when you're trying to secure the most favorable terms possible for your debt consolidation.

Top Lenders Offering No Origination Fee Debt Consolidation Loans Our Picks

Finding lenders that consistently offer no origination fees can be a bit of a treasure hunt, as policies can change. However, several reputable lenders are known for their borrower-friendly terms, often including no origination fees for qualified applicants. It's always crucial to verify the most current terms directly with the lender, but here are some of our top picks that frequently offer this benefit:

SoFi Personal Loans for Debt Consolidation

SoFi is a popular choice for debt consolidation, particularly for borrowers with good to excellent credit. They are well-known for offering personal loans with no origination fees, no late fees, and no prepayment penalties. This makes them a very attractive option for those looking to consolidate debt without hidden costs. SoFi offers competitive interest rates, often starting in the single digits for highly qualified borrowers, and loan amounts can go up to $100,000, making them suitable for larger debt consolidation needs. Their application process is entirely online, and they offer a pre-qualification option that allows you to check your rates without impacting your credit score. SoFi also provides unemployment protection, which can be a valuable safety net if you lose your job. Their customer service is generally highly rated, and they offer a range of financial products beyond personal loans, fostering a holistic financial approach for their members.

SoFi Product Comparison and Use Cases

- Loan Amounts: $5,000 to $100,000

- Interest Rates: Typically 8.99% to 29.99% APR (as of late 2023/early 2024, subject to change)

- Fees: No origination fees, no late fees, no prepayment penalties.

- Credit Score Requirement: Generally good to excellent (680+)

- Use Case: Ideal for individuals with strong credit looking to consolidate a significant amount of high-interest credit card debt or multiple personal loans. Their high loan limits make them suitable for larger consolidation projects.

- Pricing Insight: While the lowest rates are reserved for the best credit profiles, the absence of fees means the quoted APR is truly what you pay, making it easier to budget.

LightStream Personal Loans for Debt Consolidation

LightStream, a division of Truist Bank, is another excellent option for borrowers with strong credit. They pride themselves on offering a 'Loan Experience You Can Bank On,' and a key part of that is their commitment to no fees whatsoever – no origination fees, no prepayment penalties, and no late fees. LightStream is known for its highly competitive interest rates, often among the lowest in the industry, especially for borrowers with excellent credit. They offer a wide range of loan purposes, including debt consolidation, and their application process is streamlined and fully online. One unique feature of LightStream is their 'Rate Beat Program,' where they claim to beat a competitor's rate if you meet certain conditions. This commitment to competitive pricing, combined with zero fees, makes them a top contender for savvy borrowers.

LightStream Product Comparison and Use Cases

- Loan Amounts: $5,000 to $100,000

- Interest Rates: Typically 7.49% to 25.49% APR (as of late 2023/early 2024, subject to change)

- Fees: Absolutely no fees of any kind.

- Credit Score Requirement: Excellent credit (700+) and a strong credit history are usually required.

- Use Case: Best for individuals with excellent credit and a long, positive credit history who want the absolute lowest possible interest rate and no fees. Perfect for consolidating various types of debt, from credit cards to medical bills.

- Pricing Insight: LightStream's rates are often the benchmark for low-cost personal loans. If you qualify, you're likely getting one of the best deals available.

Marcus by Goldman Sachs Personal Loans for Debt Consolidation

Marcus by Goldman Sachs has quickly become a popular choice for personal loans, including debt consolidation, due to its transparent fee structure and competitive rates. They explicitly state no origination fees, no prepayment fees, and no late fees. Marcus focuses on providing a straightforward and user-friendly experience. They offer fixed-rate loans with predictable monthly payments, which is ideal for debt consolidation. While their maximum loan amount is slightly lower than SoFi or LightStream, it's still substantial enough for most debt consolidation needs. Marcus also offers a unique feature where you can defer one payment after making 12 consecutive on-time payments, which can be a helpful flexibility in a pinch.

Marcus by Goldman Sachs Product Comparison and Use Cases

- Loan Amounts: $3,500 to $40,000

- Interest Rates: Typically 8.99% to 29.99% APR (as of late 2023/early 2024, subject to change)

- Fees: No origination fees, no late fees, no prepayment penalties.

- Credit Score Requirement: Good to excellent credit (660+)

- Use Case: A great option for individuals with good credit looking to consolidate a moderate amount of debt. Their user-friendly platform and transparent terms make them appealing for those who value simplicity and predictability.

- Pricing Insight: Their rates are competitive, and the absence of fees ensures that the APR you see is the APR you get, making budgeting straightforward.

Discover Personal Loans for Debt Consolidation

Discover, a well-known financial institution, also offers personal loans for debt consolidation with a clear no-origination-fee policy. They are transparent about their terms and aim to provide a simple application process. Discover personal loans come with fixed interest rates and fixed monthly payments, which are crucial for effective debt consolidation. They also boast no prepayment penalties, allowing you to pay off your loan early without extra charges. While their rates might not always be the absolute lowest compared to LightStream for top-tier credit, they are competitive, and their customer service is generally well-regarded. Discover also offers direct payment to creditors, which can simplify the consolidation process even further by sending funds directly to your existing debt accounts.

Discover Personal Loans Product Comparison and Use Cases

- Loan Amounts: $2,500 to $40,000

- Interest Rates: Typically 7.99% to 24.99% APR (as of late 2023/early 2024, subject to change)

- Fees: No origination fees, no late fees, no prepayment penalties.

- Credit Score Requirement: Good credit (660+)

- Use Case: Suitable for individuals with good credit looking to consolidate a range of debts, especially those who appreciate the convenience of direct payment to creditors. A solid choice for those who value a well-established financial institution.

- Pricing Insight: Competitive rates without the burden of origination fees, making them a strong contender for many borrowers.

Factors to Consider When Choosing a No Origination Fee Loan for Debt Consolidation

While avoiding origination fees is a fantastic starting point, it's not the only factor to consider when selecting a debt consolidation loan. Here are some other crucial elements to keep in mind:

Interest Rates and APR for Debt Consolidation

Even without an origination fee, the interest rate is paramount. A loan with a slightly higher interest rate but no origination fee might still be more expensive than a loan with a very low interest rate and a small origination fee, depending on the loan amount and term. Always compare the Annual Percentage Rate (APR), which includes the interest rate and any other fees (though in this case, we're aiming for zero fees). The goal is to secure the lowest possible APR to maximize your savings.

Loan Terms and Repayment Schedules for Debt Consolidation

Consider the loan term – how long you have to repay the loan. Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more interest over time. Choose a term that offers a monthly payment you can comfortably afford without stretching your budget too thin. Most lenders offer terms ranging from 24 to 84 months.

Credit Score Requirements for Debt Consolidation Loans

Lenders offering no origination fees often target borrowers with good to excellent credit. Understand the credit score requirements for each lender. If your credit score isn't stellar, you might need to explore options that are more forgiving, though these might come with higher interest rates or, in some cases, an origination fee. Always check if a lender offers pre-qualification to see your potential rates without a hard credit inquiry.

Customer Service and Lender Reputation for Debt Consolidation

A smooth debt consolidation process can be greatly influenced by the lender's customer service. Look for lenders with positive reviews regarding their support, transparency, and ease of communication. A reputable lender will make the process clear and be available to answer your questions.

Prepayment Penalties for Debt Consolidation Loans

While the lenders we've highlighted typically don't have them, always double-check for prepayment penalties. These are fees charged if you pay off your loan early. A good debt consolidation loan should allow you to pay it off as quickly as you can without incurring extra costs, further accelerating your journey to debt freedom.

How to Apply for a No Origination Fee Debt Consolidation Loan

The application process for these loans is generally straightforward and can often be completed entirely online. Here's a typical step-by-step guide:

- Check Your Credit Score: Before you start, know where you stand. Your credit score will largely determine the rates and terms you're offered. You can get free credit reports from AnnualCreditReport.com and many credit card companies or financial apps.

- Gather Your Financial Information: You'll need details about your income, employment, existing debts (account numbers, balances, interest rates), and possibly bank statements.

- Pre-qualify with Multiple Lenders: This is a crucial step. Many lenders, including those mentioned above, allow you to pre-qualify with a soft credit inquiry, which doesn't affect your credit score. This lets you compare personalized rate offers from several lenders without commitment.

- Compare Offers Carefully: Look beyond just the interest rate. Consider the APR, loan term, monthly payment, and any other fees (even though we're aiming for none!).

- Submit a Formal Application: Once you've chosen the best offer, you'll proceed with a formal application. This usually involves a hard credit inquiry, which will temporarily ding your credit score by a few points.

- Provide Documentation: The lender may request documents to verify your income, identity, and existing debts.

- Receive Funds and Pay Off Debts: Once approved, the funds will be disbursed. Some lenders can send the money directly to your creditors, simplifying the process. Otherwise, you'll be responsible for paying off your old debts yourself.

Real-World Scenarios and Success Stories with No Origination Fee Loans

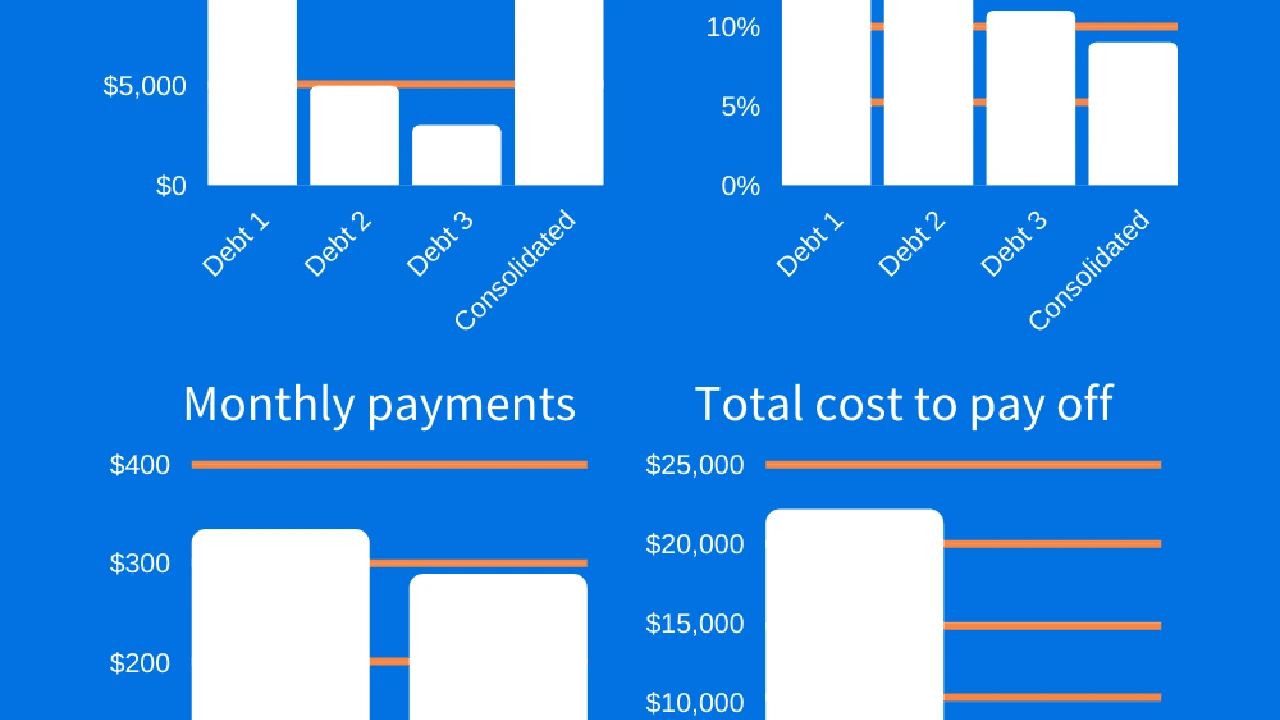

Let's look at how these loans can play out in real life. Imagine Sarah, who has $15,000 in credit card debt spread across three cards, with an average interest rate of 22%. Her minimum payments are manageable, but she's barely making a dent in the principal. She applies for a debt consolidation loan with no origination fee and is approved for a $15,000 loan at 10% APR over 60 months. Her old minimum payments totaled around $450, but her new consolidated payment is $318. Not only does she save over $130 a month, but she also saves thousands in interest over the life of the loan, and she has a clear end date for her debt. The absence of an origination fee means the full $15,000 goes directly to paying off her high-interest credit cards, maximizing her savings from day one.

Another example is Mark, a small business owner who accumulated $25,000 in personal debt from various sources, including a high-interest personal loan and some credit card balances. His credit score is good, but not excellent. He finds a lender offering a no-origination-fee loan at 12% APR. While he might have found a slightly lower rate with a different lender that charged a 3% origination fee, that fee would have cost him $750 upfront. By choosing the no-fee option, he avoids that immediate cost, and the slightly higher interest rate is offset by the immediate savings and the psychological benefit of not starting his new loan already 'down' a few hundred dollars. He uses the loan to pay off his existing debts, simplifying his monthly payments and freeing up cash flow to reinvest in his business.

Potential Downsides and What to Watch Out For

While no-origination-fee loans are generally a great deal, it's important to be aware of potential trade-offs. Sometimes, a lender might offer a no-origination-fee loan but compensate by charging a slightly higher interest rate. This isn't always the case, especially with the top lenders we've discussed, but it's why comparing the overall APR is so important. Always do the math to ensure that the total cost of the loan (interest + fees) is indeed lower than your current debt situation and better than other loan offers.

Also, remember that qualifying for these loans often requires a good to excellent credit score. If your credit isn't in that range, you might find fewer options for no-origination-fee loans, or the interest rates offered might not be as attractive. In such cases, you might need to consider other strategies, such as working on improving your credit score first, or exploring secured personal loans or credit counseling services.

Finally, be wary of lenders who advertise 'no fees' but then have hidden charges or extremely high interest rates that negate any savings. Always read the fine print of your loan agreement before signing. Transparency is key, and reputable lenders will make all terms and conditions clear upfront.

Maintaining Financial Health After Debt Consolidation

Getting a debt consolidation loan with no origination fee is a fantastic step, but it's just the beginning. The real work comes in maintaining your financial health afterward. Here are some tips:

- Stick to Your Budget: Create and adhere to a realistic budget that accounts for your new loan payment and helps you avoid accumulating new debt.

- Avoid New Debt: The primary goal of debt consolidation is to get out of debt. Resist the temptation to open new credit cards or take on unnecessary loans.

- Build an Emergency Fund: Having a financial cushion can prevent you from relying on credit cards for unexpected expenses.

- Monitor Your Credit: Regularly check your credit report for errors and monitor your score to track your progress.

- Consider Financial Education: Continue to educate yourself on personal finance best practices to make informed decisions.

By choosing a no-origination-fee debt consolidation loan, you're setting yourself up for success by minimizing upfront costs and maximizing your debt-reduction efforts. Remember to compare offers, understand the terms, and commit to responsible financial habits to truly achieve debt freedom.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)