The Impact of Debt Consolidation on Your Credit Score

Discover how consolidating your debts can affect your credit score both positively and negatively and how to manage it effectively.

Discover how consolidating your debts can affect your credit score, both positively and negatively, and how to manage it effectively.

The Impact of Debt Consolidation on Your Credit Score

Hey there! So, you're thinking about debt consolidation, right? It's a smart move for many people looking to get a handle on their finances. But one big question that often comes up is, "How will this affect my credit score?" It's a totally valid concern because your credit score is super important for everything from getting a new apartment to buying a car or even landing certain jobs. Let's dive deep into how debt consolidation can play a role in shaping your credit score, both for better and for worse, and what you can do to make sure it works in your favor.

Understanding Your Credit Score and Debt Consolidation Basics

Before we talk about the impact, let's quickly recap what a credit score is and how debt consolidation works. Your credit score is basically a three-digit number that tells lenders how risky you are as a borrower. The higher the score, the better. It's calculated based on several factors, including your payment history, amounts owed, length of credit history, new credit, and credit mix.

Debt consolidation, in a nutshell, is when you take multiple debts – like credit card balances, personal loans, or medical bills – and combine them into a single, new loan. The goal is usually to get a lower interest rate, a single monthly payment, and a clearer path to becoming debt-free. Common methods include personal loans, balance transfer credit cards, and home equity loans.

The Positive Effects of Debt Consolidation on Your Credit Score

When done right, debt consolidation can actually give your credit score a nice boost. Here’s how:

Improved Payment History and On-Time Payments

This is probably the biggest positive. Payment history accounts for a whopping 35% of your FICO score. If you've been struggling to keep up with multiple payments, missing due dates, or making late payments, your credit score has likely taken a hit. Consolidating your debts into one manageable payment makes it much easier to pay on time, every time. As you consistently make on-time payments on your new consolidated loan, your payment history will improve, and your credit score will start to climb.

Reduced Credit Utilization Ratio and Available Credit

Your credit utilization ratio (CUR) is the amount of credit you're using compared to your total available credit. It's another significant factor, making up about 30% of your FICO score. Lenders like to see a low CUR, ideally below 30%. When you consolidate high-interest credit card debt, you're essentially paying off those credit card balances. This dramatically lowers your CUR on those cards, which can instantly improve your credit score. Even if you close the old accounts (which we'll discuss later), the immediate reduction in utilized credit can be beneficial.

Simplified Debt Management and Financial Stress Reduction

While not directly a credit score factor, reduced financial stress and simplified debt management indirectly contribute to a better credit score. When you're less stressed about juggling multiple bills, you're more likely to make sound financial decisions and stay on top of your payments. This consistency is key to a healthy credit profile.

The Potential Negative Effects of Debt Consolidation on Your Credit Score

It's not all sunshine and rainbows, though. Debt consolidation can also have some temporary or even long-term negative impacts on your credit score if you're not careful. It's crucial to be aware of these so you can mitigate them.

Temporary Dip from Hard Inquiries and New Credit Accounts

When you apply for a new loan or a balance transfer credit card, lenders will typically perform a 'hard inquiry' on your credit report. A hard inquiry is a request for your credit report that happens when you apply for new credit. Each hard inquiry can cause a small, temporary dip in your credit score, usually by a few points. While a single inquiry isn't a big deal, multiple inquiries in a short period can add up. However, credit scoring models often treat multiple inquiries for the same type of loan (like personal loans) within a short window (usually 14-45 days) as a single inquiry, recognizing you're rate shopping. So, try to do your loan shopping within a concentrated period.

Opening a new credit account also slightly lowers the average age of your credit accounts, which can have a minor negative impact. This factor accounts for about 15% of your FICO score.

Closing Old Credit Card Accounts and Credit History Length

After consolidating, you might be tempted to close your old credit card accounts. While this might feel like a good idea to prevent future spending, it can actually hurt your credit score. Closing old accounts reduces your total available credit, which can increase your credit utilization ratio if you still carry balances elsewhere. More importantly, it shortens your average length of credit history, especially if those were your oldest accounts. A longer credit history generally looks better to lenders. It's often better to keep old accounts open, even if you cut up the cards and don't use them, as long as they don't have annual fees.

Risk of Accumulating New Debt and Increased Debt Burden

This is perhaps the biggest danger. Debt consolidation frees up your credit lines. If you don't address the underlying spending habits that led to debt in the first place, you might be tempted to use those newly available credit cards again. If you consolidate your old debt and then rack up new debt on your old cards, you'll end up in a worse position than before, with even more debt and a potentially damaged credit score. This is why a strong budget and financial discipline are absolutely critical after consolidation.

Specific Debt Consolidation Products and Their Credit Impact

The type of debt consolidation product you choose can also influence its impact on your credit score. Let's look at some common options:

Personal Loans for Debt Consolidation

How it works: You get a new, unsecured loan from a bank, credit union, or online lender and use the funds to pay off your existing debts. You then make one fixed monthly payment to the personal loan lender.

Credit Impact:

- Positive: Improves payment history, lowers credit utilization (by paying off revolving credit), and diversifies your credit mix (adding an installment loan).

- Negative: Hard inquiry, new account lowers average age of accounts.

Product Recommendations & Scenarios:

- LightStream: Known for competitive rates for borrowers with excellent credit (typically 700+ FICO). They offer loans from $5,000 to $100,000 with terms from 24 to 84 months. Scenario: You have a FICO score of 760, multiple credit cards with high balances, and want a fixed payment and lower interest rate. LightStream could offer you a rate as low as 5.99% APR.

- SoFi: Good for borrowers with good to excellent credit (680+ FICO). Offers loans up to $100,000 with flexible terms. They also have unemployment protection. Scenario: You have a FICO score of 700, stable income, and want a lender with good customer service and potential for unemployment benefits if needed. SoFi might offer rates starting around 7.99% APR.

- Marcus by Goldman Sachs: Offers personal loans with no fees (origination, late, or prepayment). Good for borrowers with good credit (660+ FICO). Loans from $3,500 to $40,000. Scenario: You have a FICO score of 680, want to avoid all fees, and need a loan for around $15,000 to consolidate credit card debt. Marcus could be a great fit, with rates potentially from 8.99% APR.

- Upgrade: More accessible for fair credit (600+ FICO). Offers loans from $1,000 to $50,000. They also offer a credit line product. Scenario: Your FICO score is 630, and you're struggling to get approved elsewhere. Upgrade might approve you, though rates will be higher, perhaps starting at 12.99% APR.

Balance Transfer Credit Cards for Debt Consolidation

How it works: You transfer balances from high-interest credit cards to a new credit card that offers a 0% introductory APR for a set period (e.g., 12-21 months). You pay off the principal during this period.

Credit Impact:

- Positive: Significantly lowers credit utilization on old cards, potentially increasing your overall available credit if the new card has a high limit.

- Negative: Hard inquiry, new account lowers average age of accounts. If you don't pay off the balance before the intro period ends, the interest rate can jump significantly, potentially leading to more debt. There's often a balance transfer fee (typically 3-5%).

Product Recommendations & Scenarios:

- Chase Slate Edge: Offers a 0% intro APR for 18 months on purchases and balance transfers. No annual fee. Balance transfer fee of 3% intro, then 5%. Scenario: You have excellent credit (740+ FICO) and can realistically pay off a $5,000 credit card balance within 18 months. This card gives you a long interest-free period.

- Citi Simplicity Card: Known for one of the longest 0% intro APR periods – 21 months on balance transfers and 12 months on purchases. No late fees, no annual fee. Balance transfer fee of 3% intro, then 5%. Scenario: You have good credit (680+ FICO) and need a very long time to pay off a larger balance, say $8,000, without interest.

- Wells Fargo Reflect Card: Offers 0% intro APR for 21 months on purchases and qualifying balance transfers. No annual fee. Balance transfer fee of 3% intro, then 5%. Scenario: Similar to Citi Simplicity, if you have good credit (680+ FICO) and need an extended interest-free period for a balance of $7,000.

Home Equity Loans or HELOCs for Debt Consolidation

How it works: You borrow against the equity in your home. A home equity loan is a lump sum, while a Home Equity Line of Credit (HELOC) is a revolving line of credit. These are secured loans.

Credit Impact:

- Positive: Can offer very low interest rates, especially compared to unsecured debt. Improves credit mix by adding a secured installment loan.

- Negative: Hard inquiry, new account. The biggest risk is that your home is collateral. If you default, you could lose your home. This is a significant risk to consider.

Product Recommendations & Scenarios:

- Bank of America Home Equity Loan/HELOC: Offers competitive rates and various terms. Scenario: You own a home with significant equity (e.g., $100,000 in equity on a $300,000 home), have excellent credit (720+ FICO), and a large amount of high-interest debt ($30,000+) that you want to consolidate into a lower-rate, tax-deductible (in some cases) loan.

- PNC Bank Home Equity Line of Credit: Known for flexible options and competitive rates. Scenario: You have good credit (680+ FICO), substantial home equity, and prefer the flexibility of a HELOC to draw funds as needed, perhaps to pay off debts gradually or for other expenses.

Debt Management Plans (DMPs) through Credit Counseling

How it works: A non-profit credit counseling agency negotiates with your creditors to lower interest rates and waive fees. You make one monthly payment to the agency, which then distributes the funds to your creditors.

Credit Impact:

- Positive: Improves payment history, as you make consistent payments.

- Negative: Creditors might mark your accounts as 'managed' or 'closed by grantor,' which can be viewed negatively by some lenders. Your credit score might dip initially and take time to recover. It doesn't reduce your credit utilization in the same way a loan does.

Product Recommendations & Scenarios:

- National Foundation for Credit Counseling (NFCC) members: These are reputable non-profit agencies. Scenario: You have significant credit card debt, a lower credit score (e.g., 580-650 FICO), and are struggling to make minimum payments. You need help negotiating with creditors and want a structured repayment plan without taking on a new loan.

Strategies to Maximize Positive Credit Impact and Minimize Negatives

Okay, so you know the good and the bad. Now, how do you make sure debt consolidation helps your credit score in the long run?

1. Research and Compare Lenders Carefully

Don't just jump at the first offer. Shop around for the best rates and terms. Many lenders offer pre-qualification with a 'soft inquiry,' which doesn't affect your credit score. Use this to compare offers before committing to a hard inquiry. Look for lenders with transparent fees and good customer reviews.

2. Keep Old Credit Accounts Open (If Possible)

As mentioned, closing old, paid-off credit card accounts can hurt your credit score by reducing your total available credit and shortening your credit history. If the cards don't have annual fees, it's generally better to keep them open, even if you put them away and don't use them. This helps maintain a low credit utilization ratio and a long credit history.

3. Make All Payments On Time, Every Time

This is non-negotiable. The primary benefit of debt consolidation for your credit score is the ability to make consistent, on-time payments. Set up automatic payments if you can, or use reminders to ensure you never miss a due date on your new consolidated loan.

4. Avoid Taking on New Debt

This is critical. Debt consolidation is a tool to help you get out of debt, not an excuse to accumulate more. If you pay off your credit cards and then immediately start charging them up again, you'll be in a worse financial situation and your credit score will suffer. Focus on changing your spending habits and sticking to a budget.

5. Monitor Your Credit Report Regularly

After consolidating, keep a close eye on your credit report. You can get a free copy from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once a year at AnnualCreditReport.com. Check for any errors and ensure your old accounts are reported as paid off or with zero balances. Many credit card companies and banks also offer free credit score monitoring services.

6. Build an Emergency Fund

One of the reasons people fall into debt is unexpected expenses. Once you've consolidated and have a more manageable payment, prioritize building an emergency fund. Aim for at least 3-6 months of living expenses. This way, if an unexpected bill pops up, you won't have to rely on credit cards again.

7. Understand the Underlying Causes of Your Debt

Debt consolidation is a symptom solver, not a cure for the root cause of debt. Take time to understand why you accumulated debt in the first place. Was it overspending, job loss, medical emergencies, or something else? Addressing these underlying issues is crucial for long-term financial health and a consistently good credit score.

Real-World Scenarios and Credit Score Outcomes

Let's look at a couple of hypothetical situations to illustrate the credit score impact:

Scenario 1: The Disciplined Consolidator

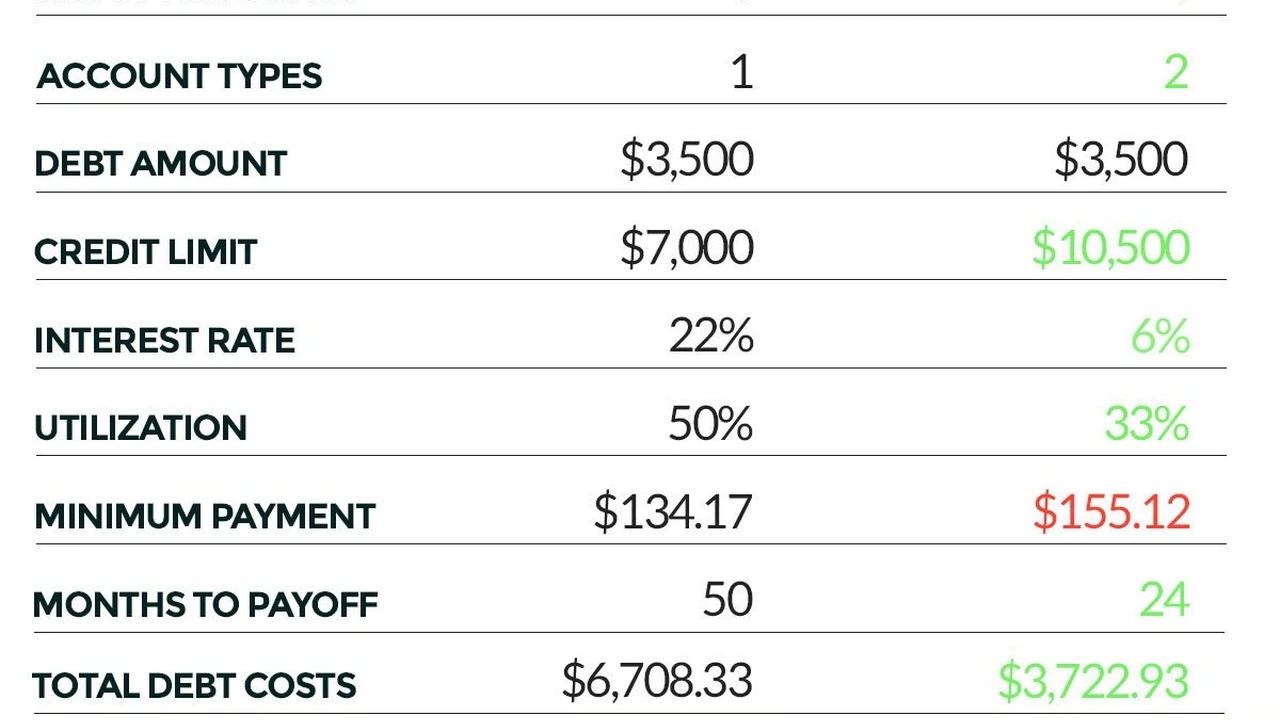

Sarah has $15,000 in credit card debt spread across three cards, with an average interest rate of 20%. Her FICO score is 680. She applies for a personal loan for debt consolidation. This results in one hard inquiry and a new account on her report, causing a temporary dip of about 5 points. However, she uses the loan to pay off all three credit cards, bringing their balances to zero. Her credit utilization ratio drops from 80% to 0% on those cards. She keeps the old credit card accounts open but doesn't use them. She diligently makes her personal loan payments on time for the next year. Her FICO score steadily increases, eventually reaching 720, thanks to improved payment history and a much lower credit utilization ratio.

Scenario 2: The Relapsing Spender

Mark has $10,000 in credit card debt and a FICO score of 620. He gets a balance transfer credit card with a 0% intro APR for 15 months. This causes a hard inquiry and a new account. He transfers his balances, and his old cards show zero balances. Initially, his score might see a small bump from the lower utilization. However, Mark doesn't change his spending habits. Within six months, he's charged up his old credit cards again, and he's also struggling to make payments on the new balance transfer card. When the 0% intro APR expires, he's hit with a high interest rate on the remaining balance. His credit utilization ratio skyrockets across all cards, and he starts missing payments. His FICO score plummets to below 580, leaving him in a worse financial state than before.

Final Thoughts on Debt Consolidation and Your Credit

Debt consolidation is a powerful tool that can significantly improve your financial situation and, by extension, your credit score. However, it's not a magic bullet. Its success hinges on your commitment to responsible financial habits. By understanding how it affects your credit, choosing the right product, and maintaining discipline, you can use debt consolidation to build a stronger credit profile and achieve lasting financial freedom. Remember, it's a marathon, not a sprint, and consistent good habits are what truly make the difference.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)