Debt Consolidation for Beginners Your First Steps to Financial Freedom

A beginner's guide to debt consolidation covering essential information and initial steps to start your journey towards debt relief.

A beginner's guide to debt consolidation covering essential information and initial steps to start your journey towards debt relief.

Debt Consolidation for Beginners Your First Steps to Financial Freedom

Hey there! Are you feeling overwhelmed by a mountain of debt? Juggling multiple payments, high-interest rates, and constantly worrying about your financial future? You're not alone. Millions of people face similar challenges, and the good news is there's a powerful tool that can help you regain control: debt consolidation. Think of it as hitting the reset button on your finances. Instead of several small, confusing debts, you combine them into one manageable payment, often with a lower interest rate. This guide is your friendly starting point, designed to walk you through the basics, explore some real-world options, and help you take those crucial first steps toward financial freedom.

Understanding Debt Consolidation What It Is and How It Works

So, what exactly is debt consolidation? In simple terms, it's the process of taking out a new loan or credit facility to pay off several existing debts. Instead of owing money to multiple creditors (like credit card companies, personal loan providers, or medical billers), you'll owe money to just one. This simplifies your monthly payments, making it easier to track your progress and avoid missing due dates. But it's not just about convenience; often, the new consolidated loan comes with a lower interest rate than the average of your previous debts. This means more of your payment goes towards the principal balance, helping you pay off your debt faster and save a significant amount of money in interest over time.

Let's break down how it typically works:

- Assess Your Debts: First, you'll list all your outstanding debts, including credit cards, personal loans, medical bills, and any other unsecured debts. Note down the principal amount, interest rate, and minimum monthly payment for each.

- Choose a Consolidation Method: This is where you decide which type of consolidation product is best for you (we'll dive into specific products shortly!). Common methods include personal loans, balance transfer credit cards, and home equity loans.

- Apply for the New Product: You apply for the chosen consolidation product. The lender will review your credit history, income, and debt-to-income ratio to determine your eligibility and the interest rate they can offer.

- Pay Off Old Debts: If approved, the funds from your new loan or credit line are used to pay off your existing debts. This is often done directly by the new lender, or you might receive the funds to pay them off yourself.

- Make One New Payment: Now, instead of multiple payments, you'll make a single, regular payment to your new lender. This payment will typically be fixed, making budgeting much simpler.

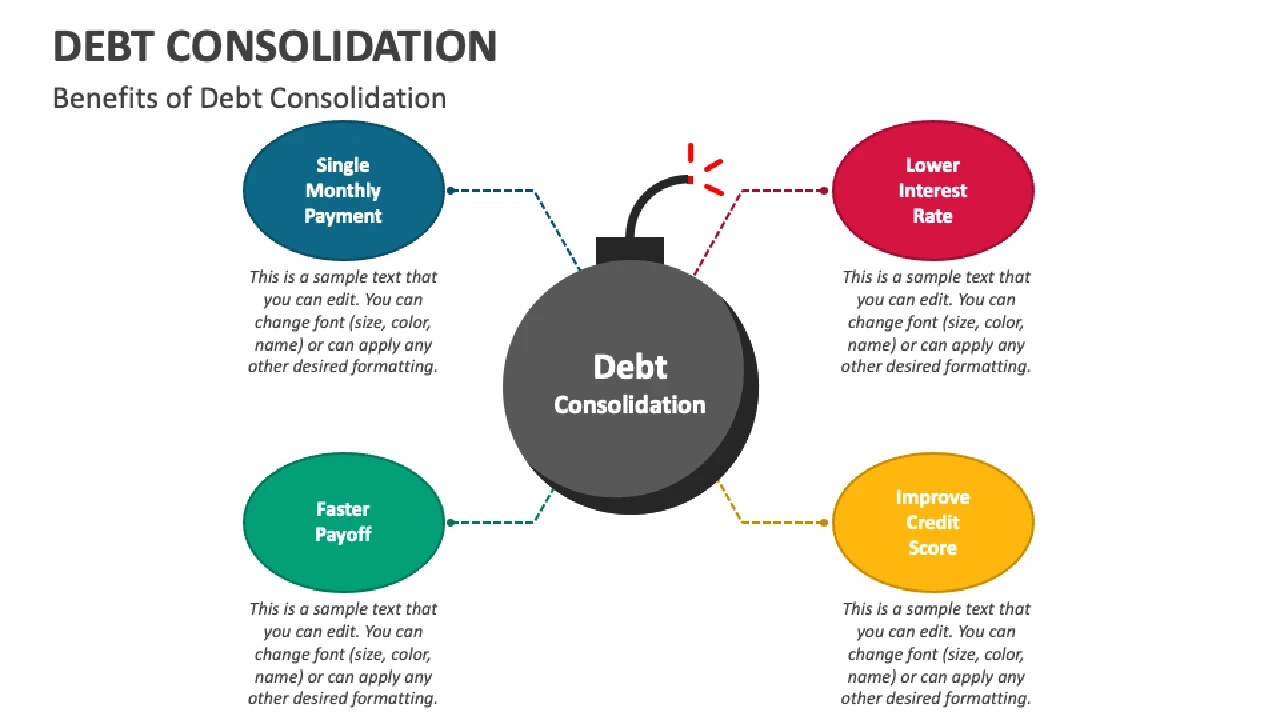

Key Benefits of Debt Consolidation Simplifying Your Finances

Why should you even consider debt consolidation? The benefits can be substantial, especially if you're struggling with high-interest, scattered debts:

- Lower Interest Rates: This is often the biggest draw. If you can secure a consolidation loan with a lower interest rate than your current average, you'll save money and pay off your debt faster.

- Simplified Payments: One payment instead of many. This reduces the mental load, minimizes the risk of missed payments, and makes budgeting a breeze.

- Clearer Path to Debt Freedom: With a single, fixed payment and a set repayment schedule, you can clearly see when you'll be debt-free. This provides motivation and a sense of control.

- Potential for Lower Monthly Payments: While not always the case, consolidating can sometimes result in a lower overall monthly payment, freeing up cash flow for other necessities or savings. Be cautious here, as a lower payment might mean a longer repayment period, potentially increasing total interest paid.

- Improved Credit Score (Eventually): By consistently making on-time payments on your consolidated loan, you can positively impact your credit score over time. Closing old credit card accounts (after paying them off) can also reduce your credit utilization ratio, which is good for your score.

Popular Debt Consolidation Products A Look at Your Options

Alright, let's get into the nitty-gritty of the actual products you can use for debt consolidation. Each has its own pros and cons, and the best choice for you will depend on your credit score, the amount of debt you have, and your financial goals.

Personal Loans for Debt Consolidation Unsecured and Flexible

Personal loans are one of the most common and straightforward ways to consolidate debt. These are typically unsecured loans, meaning you don't need to put up collateral like your home or car. You borrow a lump sum, use it to pay off your existing debts, and then make fixed monthly payments over a set period (usually 2-7 years).

Who It's Best For:

- Individuals with good to excellent credit scores (this will get you the best interest rates).

- Those who prefer a fixed monthly payment and a clear end date for their debt.

- People with various types of unsecured debt (credit cards, medical bills, other personal loans).

Things to Consider:

- Interest Rates: These can range from around 6% to 36%, depending heavily on your creditworthiness.

- Origination Fees: Some lenders charge an upfront fee (typically 1-8% of the loan amount) that's deducted from your loan proceeds.

- Loan Amounts: Usually range from $1,000 to $100,000.

Recommended Products and Scenarios:

When looking for personal loans, online lenders often offer competitive rates and a streamlined application process. Here are a few popular options:

LightStream Personal Loans

- Best For: Borrowers with excellent credit (typically 700+ FICO score) looking for the lowest rates.

- Key Features: Offers some of the lowest APRs in the industry (starting around 6-7% for debt consolidation, depending on loan term and credit profile). No origination fees. Flexible loan amounts from $5,000 to $100,000. Repayment terms from 24 to 84 months.

- Usage Scenario: Imagine you have $25,000 in credit card debt spread across three cards, with an average APR of 18%. If you qualify for a LightStream loan at 8% APR over 60 months, your monthly payment would be significantly lower, and you'd save thousands in interest.

- Pricing/Rates: APRs from 6.99% to 23.99% with AutoPay. Rates vary based on loan purpose, amount, term, and creditworthiness.

SoFi Personal Loans

- Best For: Good to excellent credit borrowers (typically 680+ FICO) who value unemployment protection and career support.

- Key Features: Competitive fixed rates, no origination fees, no late fees, and no prepayment penalties. Offers unemployment protection, allowing you to pause payments if you lose your job. Loan amounts from $5,000 to $100,000. Repayment terms from 24 to 84 months.

- Usage Scenario: You have $15,000 in various debts, including a medical bill and a high-interest store card. SoFi could offer a competitive rate, and their unemployment protection provides peace of mind if your job situation is uncertain.

- Pricing/Rates: APRs from 8.99% to 29.99% with AutoPay. Rates depend on credit score, income, and other factors.

Marcus by Goldman Sachs Personal Loans

- Best For: Good credit borrowers (typically 660+ FICO) seeking a straightforward loan with no fees.

- Key Features: No origination fees, no late fees, and no prepayment penalties. Offers a 0.25% APR reduction for making 12 consecutive on-time payments. Loan amounts from $3,500 to $40,000. Repayment terms from 36 to 72 months.

- Usage Scenario: You have $10,000 in credit card debt and want a simple, no-frills loan to consolidate. Marcus's lack of fees and potential rate reduction for good payment behavior make it an attractive option.

- Pricing/Rates: APRs from 8.99% to 29.99%. Rates depend on creditworthiness and loan term.

Balance Transfer Credit Cards for Debt Consolidation Zero Percent APR Offers

Balance transfer credit cards can be a fantastic option if you have primarily credit card debt and a good credit score. These cards offer an introductory 0% APR period (typically 12 to 21 months) on transferred balances. This means that for the entire promotional period, 100% of your payments go directly to reducing your principal, not interest.

Who It's Best For:

- Individuals with good to excellent credit (usually 670+ FICO) to qualify for the best offers.

- Those who are disciplined enough to pay off the transferred balance entirely before the 0% APR period ends.

- People with manageable amounts of credit card debt that can realistically be paid off within the promotional window.

Things to Consider:

- Balance Transfer Fees: Most cards charge a fee for transferring a balance, typically 3-5% of the transferred amount. This is a one-time fee.

- Promotional Period: Be acutely aware of when the 0% APR period ends. After that, any remaining balance will accrue interest at the card's standard (often high) APR.

- Credit Limit: The new card's credit limit needs to be high enough to cover the debt you want to transfer.

Recommended Products and Scenarios:

The key with balance transfer cards is to find one with a long 0% APR period and a reasonable transfer fee. Here are some top contenders:

Citi Simplicity Card

- Best For: Those needing a very long 0% APR period and no late fees.

- Key Features: Offers one of the longest 0% intro APR periods on balance transfers (often 21 months). No annual fee, no late fees, and no penalty rate.

- Usage Scenario: You have $8,000 in credit card debt and are confident you can pay it off within 21 months. The Citi Simplicity card allows you to make significant progress without any interest charges, and the absence of late fees provides a small buffer if you accidentally miss a payment (though you should always aim to pay on time!).

- Pricing/Rates: 0% intro APR on balance transfers for 21 months from date of first transfer. After that, a variable APR of 19.24% - 29.99%. Balance transfer fee of 5% (minimum $5).

Chase Slate Edge

- Best For: Borrowers who want a 0% intro APR and a chance to lower their ongoing APR.

- Key Features: 0% intro APR on purchases and balance transfers for 18 months. After the intro period, you can automatically be considered for an APR reduction by spending $1,000 and paying on time. No annual fee.

- Usage Scenario: You have $6,000 in credit card debt and want a solid 0% intro period. The potential to lower your ongoing APR after the intro period is a nice bonus if you don't quite pay off the full balance.

- Pricing/Rates: 0% intro APR on purchases and balance transfers for 18 months. After that, a variable APR of 20.49% - 29.24%. Balance transfer fee of 3% for transfers made within 60 days of account opening, then 5%.

Wells Fargo Reflect Card

- Best For: Those seeking a long 0% intro APR period with an option to extend it.

- Key Features: Offers a 0% intro APR for 18 months, which can be extended for an additional 3 months if you make on-time minimum payments during the intro period. No annual fee.

- Usage Scenario: You have $12,000 in credit card debt and need as much time as possible to pay it down interest-free. The potential to extend the 0% APR period to 21 months with good payment behavior is a significant advantage.

- Pricing/Rates: 0% intro APR for 18 months from account opening on purchases and qualifying balance transfers. Extend for up to 3 months with on-time minimum payments. After that, a variable APR of 18.24% - 30.24%. Balance transfer fee of 5% (minimum $5).

Home Equity Loans or HELOCs for Debt Consolidation Secured Options

If you own a home and have significant equity, a home equity loan or a Home Equity Line of Credit (HELOC) can be a powerful debt consolidation tool. These are secured loans, meaning your home serves as collateral. Because they're secured, they typically offer much lower interest rates than unsecured personal loans or credit cards.

Who It's Best For:

- Homeowners with substantial equity in their home.

- Individuals with a large amount of high-interest debt.

- Those who are confident in their ability to make payments, understanding the risk of using their home as collateral.

Things to Consider:

- Risk: This is the biggest factor. If you default on a home equity loan, you could lose your home.

- Closing Costs: Like a mortgage, these loans often come with closing costs (appraisal fees, origination fees, etc.), which can add up.

- Interest Rates: Generally much lower than unsecured options, but can be fixed (home equity loan) or variable (HELOC).

Recommended Products and Scenarios:

Home equity products are typically offered by traditional banks and credit unions. The best option often depends on your existing mortgage lender or local financial institutions.

Bank of America Home Equity Loan

- Best For: Homeowners seeking a fixed interest rate and predictable monthly payments.

- Key Features: Fixed interest rates for the life of the loan, predictable monthly payments. Loan amounts typically from $10,000 up to a percentage of your home's equity. Repayment terms often 10, 15, or 20 years.

- Usage Scenario: You have $50,000 in various high-interest debts and significant home equity. A Bank of America Home Equity Loan could offer a much lower, fixed interest rate, making your monthly payments predictable and potentially much lower than your combined previous payments.

- Pricing/Rates: Rates vary significantly based on credit score, loan-to-value (LTV), loan amount, and term. Expect rates to be in the single digits for well-qualified borrowers. Closing costs typically apply.

Chase Home Equity Line of Credit (HELOC)

- Best For: Homeowners who need flexible access to funds and prefer a variable interest rate.

- Key Features: A revolving line of credit, similar to a credit card, but secured by your home. You only pay interest on the amount you borrow. Variable interest rates. Draw period (typically 10 years) followed by a repayment period (typically 20 years).

- Usage Scenario: You have fluctuating debt or anticipate needing funds for other purposes in addition to consolidation. A Chase HELOC allows you to draw funds as needed to pay off debts, and then repay them, with the flexibility to draw again if necessary (during the draw period).

- Pricing/Rates: Variable APRs, often tied to the prime rate. Rates can start in the high single digits. Closing costs may apply, though some lenders offer promotions to waive them.

Initial Steps to Take Before Consolidating Your Debt Preparing for Success

Before you jump into applying for any of these products, there are a few crucial steps you should take to ensure you're making the best decision and setting yourself up for success.

Review Your Credit Report and Score Understanding Your Financial Health

Your credit score is a huge factor in determining what interest rates and loan products you'll qualify for. Get a free copy of your credit report from AnnualCreditReport.com (you're entitled to one free report from each of the three major bureaus annually). Review it carefully for any errors and dispute them. Knowing your credit score (you can often get this for free from your bank or credit card company) will give you a realistic idea of your options.

Calculate Your Total Debt and Average Interest Rate Knowing Your Numbers

List every single debt you want to consolidate. For each, note the current balance, the interest rate, and the minimum monthly payment. Then, calculate your total debt and the weighted average interest rate. This will help you determine if a consolidation loan's interest rate is truly better than what you're currently paying.

Create a Realistic Budget Post Consolidation Planning Your Payments

Debt consolidation isn't a magic bullet; it's a tool. For it to work, you need a solid budget. Figure out how much you can realistically afford to pay each month towards your consolidated debt. This new payment should be sustainable and allow you to live comfortably without accumulating new debt. Use budgeting apps or a simple spreadsheet to track your income and expenses.

Understand the Risks and Rewards Weighing Your Options Carefully

Every financial decision has risks. With debt consolidation, the main risks include:

- Extending Repayment Time: A lower monthly payment might mean a longer repayment period, potentially increasing the total interest you pay over the life of the loan.

- Accumulating New Debt: If you consolidate and then run up new debt on your now-empty credit cards, you'll be in a worse position than before.

- Using Your Home as Collateral: With home equity loans, you risk foreclosure if you can't make payments.

Be honest with yourself about your spending habits and commitment to change.

Making the Right Choice for Your Debt Consolidation Journey Personalized Advice

Choosing the right debt consolidation method is a personal decision. There's no one-size-fits-all answer. Here's a quick guide to help you think through it:

- If you have excellent credit and manageable credit card debt: A balance transfer credit card with a long 0% APR period might be your best bet. Just be sure you can pay it off before the promotional period ends.

- If you have good to excellent credit and various types of unsecured debt: A personal loan is likely a strong contender. It offers a fixed payment and a clear end date.

- If you have significant home equity and a large amount of high-interest debt: A home equity loan or HELOC could offer the lowest interest rates, but remember the risk involved.

- If your credit isn't great: Your options might be more limited, and interest rates higher. You might need to focus on improving your credit score first, or explore alternatives like a debt management plan through a credit counseling agency.

Don't be afraid to shop around! Get quotes from multiple lenders for personal loans, check different balance transfer offers, and compare terms. Many lenders offer pre-qualification processes that allow you to see potential rates without impacting your credit score.

Beyond Consolidation Building a Debt-Free Future

Remember, debt consolidation is a fresh start, not a finish line. Once you've consolidated your debts, the real work begins: changing the habits that led to debt in the first place. This means sticking to your budget, avoiding new unnecessary debt, and building an emergency fund. Think of this as an opportunity to build a healthier relationship with money and pave the way for true financial freedom. You've got this!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)