Debt Consolidation vs Debt Management Plans What's the Difference

Learn the distinctions between debt consolidation and debt management plans to choose the most effective approach for your debt relief.

Learn the distinctions between debt consolidation and debt management plans to choose the most effective approach for your debt relief.

Debt Consolidation vs Debt Management Plans Whats the Difference

Navigating the world of debt relief can feel like deciphering a complex financial puzzle. When you're looking for ways to get out from under a mountain of bills, two terms often pop up: debt consolidation and debt management plans. While both aim to help you manage and reduce your debt, they are distinct strategies with different approaches, implications, and suitability for various financial situations. Understanding these differences is crucial for making an informed decision that aligns with your financial goals and current circumstances. Let's dive deep into what each entails, how they work, and which might be the better fit for you.

Understanding Debt Consolidation Your Path to Simplified Payments

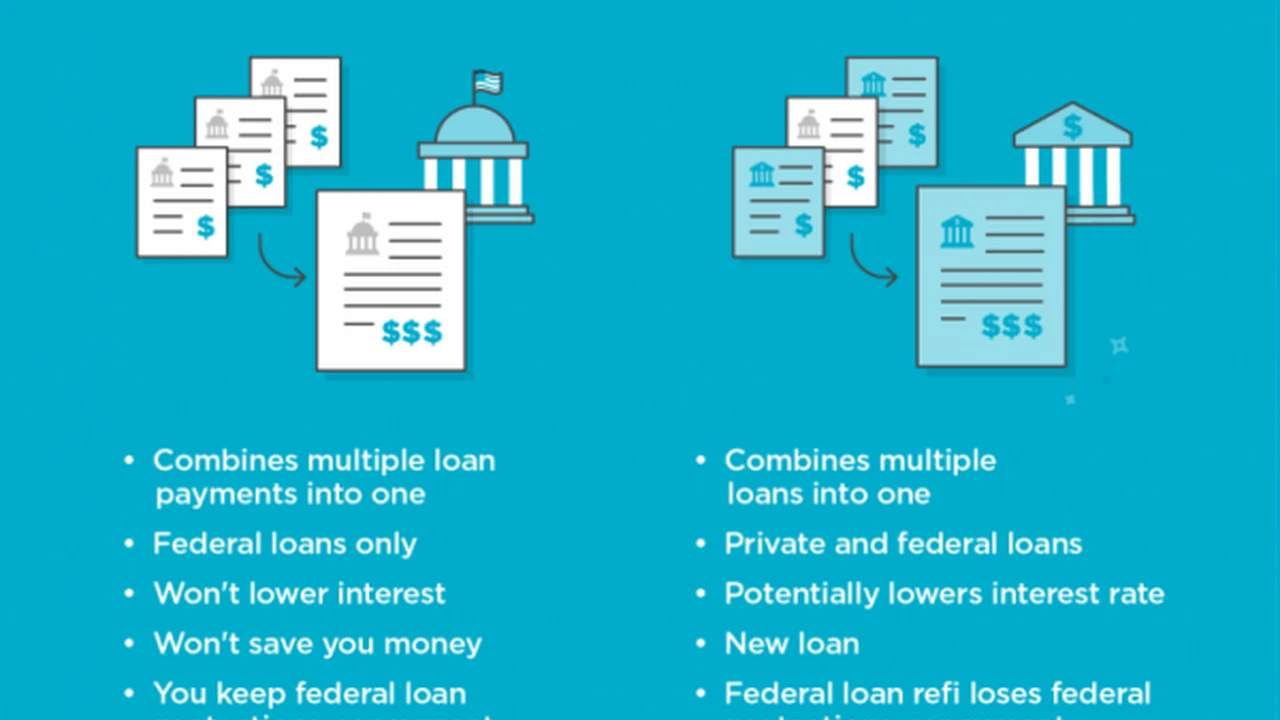

Debt consolidation is essentially taking out a new, larger loan to pay off several smaller debts. The goal is to combine multiple debts—like credit card balances, personal loans, or medical bills—into a single, more manageable payment, often with a lower interest rate. This can simplify your finances, making it easier to track payments and potentially reducing your overall interest costs.

How Debt Consolidation Works Exploring Loan Types and Processes

The most common forms of debt consolidation involve:

- Personal Loans: These are unsecured loans (meaning they don't require collateral) that you can use to pay off your existing debts. If you have good credit, you might qualify for a lower interest rate than what you're currently paying on your credit cards.

- Balance Transfer Credit Cards: Some credit cards offer introductory 0% APR periods for balance transfers. You can move high-interest credit card debt to one of these cards, giving you a window to pay down the principal without accruing interest. However, be mindful of balance transfer fees and ensure you can pay off the balance before the promotional period ends.

- Home Equity Loans or HELOCs: If you own a home, you can use your home equity as collateral for a loan. These often come with lower interest rates because they're secured, but they also put your home at risk if you can't make payments.

The process typically involves applying for a new loan or credit card, getting approved, and then using the funds to pay off your existing creditors. You then make one monthly payment to the new lender.

Benefits of Debt Consolidation Streamlined Finances and Potential Savings

- Simpler Payments: Instead of juggling multiple due dates and minimum payments, you have just one to remember.

- Lower Interest Rates: If you qualify for a lower interest rate on your consolidation loan, you could save a significant amount of money over time.

- Fixed Repayment Schedule: Many consolidation loans come with a fixed repayment term, giving you a clear end date for your debt.

- Reduced Stress: Managing debt can be overwhelming. Consolidation can provide a sense of control and reduce financial anxiety.

Drawbacks of Debt Consolidation Potential Risks and Considerations

- Credit Score Requirement: To get the best rates, you generally need a good to excellent credit score. If your score is low, you might not qualify for favorable terms.

- Risk of More Debt: If you consolidate and then continue to use your old credit cards, you could end up with even more debt.

- Fees: Some loans or balance transfer cards come with origination fees or balance transfer fees that can add to the overall cost.

- Secured Debt Risk: If you use a home equity loan, you're putting your home at risk.

Exploring Debt Management Plans A Structured Approach to Debt Relief

A Debt Management Plan (DMP) is a different beast altogether. It's typically offered by non-profit credit counseling agencies. In a DMP, the counseling agency works with your creditors to negotiate lower interest rates, waive fees, and create a more affordable monthly payment plan. You make one monthly payment to the credit counseling agency, and they, in turn, distribute the funds to your creditors.

How Debt Management Plans Work Partnering with Credit Counseling Agencies

When you enroll in a DMP, a credit counselor will review your financial situation, including your income, expenses, and debts. They'll then contact your creditors to propose a repayment plan. Creditors often agree to these plans because they'd rather receive some payment than none at all. The plan usually lasts for 3 to 5 years, and during this time, you're typically advised to stop using your credit cards.

Benefits of Debt Management Plans Lower Rates and Expert Guidance

- Lower Interest Rates: Creditors often agree to reduce interest rates, making your payments more manageable and allowing more of your payment to go towards the principal.

- Waived Fees: Late fees and over-limit fees might be waived.

- One Monthly Payment: Similar to consolidation, you make a single payment to the counseling agency.

- No New Loans: You don't need to take out a new loan, which can be beneficial if your credit score isn't strong enough for consolidation.

- Credit Counseling Support: You receive guidance and education from certified credit counselors.

- Stops Collection Calls: Once you're on a DMP, collection calls from creditors usually cease.

Drawbacks of Debt Management Plans Credit Impact and Restrictions

- Credit Report Notation: While not as severe as bankruptcy, a DMP can be noted on your credit report, potentially impacting your ability to get new credit during the plan.

- Credit Card Restrictions: You'll typically need to close or stop using the credit cards included in the plan.

- Fees: Credit counseling agencies may charge a small monthly fee for their services, though non-profits often keep these minimal.

- Not All Debts Included: DMPs usually focus on unsecured debts like credit cards. Secured debts, student loans, or taxes are typically not included.

Key Differences Debt Consolidation vs Debt Management Plans at a Glance

Let's break down the core distinctions to help you see which might be a better fit:

Nature of the Solution Loan vs Negotiated Plan

Debt consolidation involves taking out a new financial product (a loan or credit card) to pay off existing debts. You're essentially shifting your debt from multiple lenders to one new lender. A DMP, on the other hand, is a structured repayment plan negotiated by a third party (a credit counseling agency) with your existing creditors. You're not taking on new debt; you're just restructuring your current debt with the help of an intermediary.

Impact on Credit Score Immediate vs Long Term

With debt consolidation, if you get a new loan, there will be a hard inquiry on your credit report, which can temporarily ding your score. However, if you manage the consolidated loan well, your score can improve over time as your debt-to-income ratio potentially decreases and you make consistent payments. A DMP can also have an impact. While it's not as damaging as bankruptcy, the fact that you're on a DMP might be noted on your credit report, and closing credit card accounts can affect your credit utilization ratio. However, successfully completing a DMP can ultimately help rebuild your credit.

Eligibility Requirements Creditworthiness and Debt Type

For debt consolidation loans, especially those with favorable interest rates, a good to excellent credit score is often a prerequisite. Lenders want to see a history of responsible borrowing. DMPs are generally more accessible to individuals with lower credit scores because they don't involve taking on new credit. The primary requirement is usually that you have unsecured debt that the counseling agency can negotiate.

Control and Flexibility Your Role in the Process

With debt consolidation, you have more direct control over the loan terms you choose, assuming you qualify. You select the lender, the loan amount, and the repayment period. With a DMP, the credit counseling agency acts as an intermediary, and while you have input, the terms are negotiated with your creditors, and you're bound by the plan they establish. You also typically lose the ability to use your credit cards during a DMP.

Which Option is Right for You Making an Informed Decision

Choosing between debt consolidation and a debt management plan depends heavily on your individual financial situation, credit health, and discipline.

When Debt Consolidation Shines Good Credit and Discipline

Debt consolidation is often a great option if:

- You have a good to excellent credit score, allowing you to qualify for a low-interest personal loan or a 0% APR balance transfer card.

- You are disciplined enough to avoid accumulating new debt once your old debts are paid off.

- You prefer to manage your debt directly with a single lender.

- You want a clear end date for your debt repayment.

When a Debt Management Plan is Preferable Struggling with High Interest and Multiple Payments

A debt management plan might be a better fit if:

- You have a significant amount of high-interest unsecured debt (primarily credit cards) and are struggling to make minimum payments.

- Your credit score isn't strong enough to qualify for a favorable debt consolidation loan.

- You need the structure and guidance of a credit counseling agency to help you stick to a budget and repayment plan.

- You are comfortable closing your credit card accounts and not using them for the duration of the plan.

- You are receiving constant collection calls and need relief.

Specific Product Recommendations and Use Cases

Let's look at some specific products and scenarios to illustrate these concepts further. Please note that interest rates, fees, and eligibility criteria are subject to change and vary by lender and individual creditworthiness. Always check the most current terms directly with the provider.

Debt Consolidation Loan Products for Excellent Credit

If you have a FICO score of 720+, you're in a strong position for excellent rates.

- LightStream Personal Loans:

- Use Case: Ideal for borrowers with excellent credit seeking competitive fixed rates and flexible loan terms for various purposes, including debt consolidation. They offer loans from $5,000 to $100,000.

- Key Features: No origination fees, no prepayment penalties. Rates can be very low, often starting in the low single digits for well-qualified borrowers.

- Considerations: Requires excellent credit history. Funds can be disbursed quickly.

- Example Scenario: Sarah has a FICO score of 780 and $25,000 in credit card debt across three cards, with an average APR of 18%. She secures a LightStream loan for $25,000 at 6.99% APR over 5 years. Her single monthly payment is significantly lower, and she saves thousands in interest.

- SoFi Personal Loans:

- Use Case: Good for high-income earners with strong credit looking for larger loan amounts and potentially unemployment protection. Loans up to $100,000.

- Key Features: No origination fees, no prepayment penalties. Offers unemployment protection, allowing you to pause payments if you lose your job.

- Considerations: Strong credit and income usually required.

- Example Scenario: Mark has a FICO score of 750 and $40,000 in various personal debts. He gets a SoFi loan at 7.5% APR over 7 years, consolidating his debts and benefiting from the unemployment protection feature as a safety net.

Balance Transfer Credit Cards for Good to Excellent Credit

These are great if you can pay off the balance within the promotional period.

- Chase Slate Edge:

- Use Case: Excellent for consolidating credit card debt with a long 0% intro APR period.

- Key Features: 0% intro APR for 18 months on balance transfers (and purchases). No annual fee. Balance transfer fee typically 3% or 5%.

- Considerations: You must pay off the balance before the intro APR expires, or high variable APRs will apply.

- Example Scenario: Emily has $10,000 on a credit card with a 22% APR. She transfers the balance to a Chase Slate Edge card, paying a 3% ($300) balance transfer fee. She now has 18 months to pay off the $10,300 without interest, saving her significant money if she sticks to a strict repayment plan.

- Citi Simplicity Card:

- Use Case: Offers one of the longest 0% intro APR periods for balance transfers, ideal for those who need more time.

- Key Features: 0% intro APR for 21 months on balance transfers (and 12 months on purchases). No late fees, no penalty rate, no annual fee. Balance transfer fee typically 3% or 5%.

- Considerations: Requires good to excellent credit.

- Example Scenario: David has $15,000 in credit card debt and needs more than 18 months to pay it off. He opts for the Citi Simplicity Card, getting 21 months interest-free, giving him more breathing room to tackle his debt.

Debt Consolidation Options for Fair to Average Credit (FICO 580-669)

Options are more limited, and rates might be higher, but still better than some credit card rates.

- Upgrade Personal Loans:

- Use Case: Accessible for borrowers with fair to good credit, offering loans for debt consolidation.

- Key Features: Loans from $1,000 to $50,000. Offers joint applications. Rates can be higher than for excellent credit, but potentially lower than high-interest credit cards.

- Considerations: Origination fees apply (2.9% to 8%).

- Example Scenario: Jessica has a FICO score of 640 and $12,000 in credit card debt with an average APR of 25%. She gets an Upgrade loan for $12,000 at 18% APR over 3 years, paying an origination fee. While the rate isn't super low, it's a significant improvement over her current credit card rates, and she gets a fixed payment.

- Avant Personal Loans:

- Use Case: Caters to borrowers with fair to average credit, providing quick funding for debt consolidation.

- Key Features: Loans from $2,000 to $35,000. Fast funding, often as soon as the next business day.

- Considerations: High APRs (up to 35.99%) and administrative fees (up to 4.75%) can make it an expensive option, but still potentially better than payday loans or some high-interest credit cards.

- Example Scenario: Robert has a FICO score of 620 and needs to consolidate $8,000 in various small debts. He qualifies for an Avant loan at 29% APR. While high, it allows him to combine his debts into one payment and avoid further late fees on multiple accounts, giving him a structured path to repayment.

Debt Management Plan Providers (Non-Profit Credit Counseling)

These agencies don't offer loans but facilitate DMPs.

- National Foundation for Credit Counseling (NFCC) Members:

- Use Case: For individuals overwhelmed by unsecured debt, struggling with high interest rates, and needing structured guidance.

- Key Features: Non-profit organizations offering free initial counseling sessions. They negotiate with creditors for lower interest rates and waived fees. One monthly payment to the agency.

- Considerations: Requires commitment to the plan, typically 3-5 years. May involve closing credit card accounts. Small monthly fees may apply.

- Example Scenario: Maria has $30,000 in credit card debt across 5 cards, with an average APR of 28%. Her credit score is 590, making consolidation loans difficult. She contacts an NFCC member agency. They negotiate her average APR down to 10% and set up a 4-year DMP with a single monthly payment she can afford. This significantly reduces her interest burden and provides a clear path out of debt.

- GreenPath Financial Wellness:

- Use Case: Similar to other NFCC members, GreenPath offers comprehensive credit counseling and debt management plans.

- Key Features: Personalized counseling, debt management plans, housing counseling, and student loan counseling. Focus on holistic financial wellness.

- Considerations: Similar to other DMPs, requires adherence to the plan and may impact credit card usage.

- Example Scenario: John is facing overwhelming credit card debt and also has questions about his student loans. GreenPath helps him set up a DMP for his credit cards and provides advice on managing his student loan payments, offering a broader financial solution.

Navigating Your Options A Step-by-Step Guide

So, how do you decide? Here's a practical approach:

Step 1 Assess Your Financial Situation and Credit Health

Pull your credit report and score. Understand your total debt amount, interest rates on each debt, and your monthly income and expenses. Be honest about your spending habits and financial discipline.

Step 2 Research and Compare Debt Consolidation Loan Offers

If your credit is good, get pre-qualified for personal loans from several lenders (like LightStream, SoFi, Upgrade, Avant). Compare interest rates, fees, and repayment terms. Look into balance transfer credit cards if your debt is primarily credit card-based and you're confident you can pay it off during the intro period.

Step 3 Consult a Non-Profit Credit Counseling Agency

Even if you're leaning towards consolidation, a free consultation with an NFCC-certified credit counselor can provide valuable insights. They can help you analyze your budget, explore all your options, and determine if a DMP is a better fit, especially if your credit isn't stellar or you need more structured support.

Step 4 Weigh the Pros and Cons for Your Specific Situation

Consider the impact on your credit, the total cost (including fees and interest), the monthly payment amount, and how each option aligns with your ability to stick to a plan. Think about whether you need the external discipline of a DMP or if you can manage a consolidation loan independently.

Step 5 Make a Decision and Commit to Your Plan

Once you've chosen, commit fully. If you consolidate, close old credit card accounts or freeze them to prevent new debt. If you enter a DMP, adhere strictly to the payment schedule and avoid using credit. The key to success with either strategy is discipline and consistent effort.

Beyond the Initial Choice Long-Term Financial Health

Regardless of whether you choose debt consolidation or a debt management plan, the ultimate goal is to achieve financial freedom and build healthier money habits. This means creating and sticking to a budget, building an emergency fund, and being mindful of your spending. Both strategies are tools to help you get there, but they require your active participation and commitment to truly transform your financial future.

Remember, there's no one-size-fits-all solution. What works for one person might not work for another. Take the time to understand your options, seek professional advice, and choose the path that best suits your unique circumstances. Your journey to becoming debt-free starts with an informed decision.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)