Using a HELOC for Debt Consolidation Advantages and Disadvantages

Assess the benefits and drawbacks of using a Home Equity Line of Credit (HELOC) for debt consolidation.

Assess the benefits and drawbacks of using a Home Equity Line of Credit (HELOC) for debt consolidation.

Using a HELOC for Debt Consolidation Advantages and Disadvantages

Hey there! Are you drowning in a sea of high-interest debt, maybe from credit cards, personal loans, or even medical bills? It's a tough spot to be in, and you're definitely not alone. Many folks are looking for smart ways to get their finances back on track, and one option that often pops up is using a Home Equity Line of Credit, or HELOC, for debt consolidation. Now, before you jump in headfirst, it's super important to understand what a HELOC is, how it works for debt consolidation, and whether it's truly the right move for your unique situation. Let's break it all down, shall we?

What Exactly is a HELOC and How Does it Work for Debt Consolidation

First things first, let's define what a HELOC is. Think of it like a credit card, but instead of being backed by your creditworthiness alone, it's secured by the equity you've built up in your home. Equity is simply the difference between what your home is worth and how much you still owe on your mortgage. So, if your home is valued at $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity. A HELOC allows you to borrow against a portion of that equity, up to a certain limit set by the lender, usually around 80-90% of your home's equity.

The 'line of credit' part is key here. Unlike a traditional loan where you get a lump sum upfront, a HELOC gives you access to a revolving credit line. This means you can borrow money as you need it, up to your approved limit, repay it, and then borrow again. It's a bit like having a flexible spending account tied to your home's value. You only pay interest on the amount you actually borrow, not the entire credit line.

So, how does this tie into debt consolidation? Well, if you have multiple high-interest debts – let's say a few credit cards with 20%+ APRs, a personal loan at 15%, and maybe some lingering medical bills – you can use the funds from your HELOC to pay off all those smaller, more expensive debts. Instead of juggling multiple payments to different creditors at varying interest rates, you'd then have just one single payment to your HELOC lender, ideally at a much lower interest rate. This can simplify your finances immensely and potentially save you a ton of money on interest over time.

The Big Advantages of Using a HELOC for Debt Consolidation

There are some really compelling reasons why a HELOC might look attractive for debt consolidation. Let's dive into the main benefits:

Lower Interest Rates and Reduced Monthly Payments with HELOC

This is often the biggest draw. Because a HELOC is secured by your home, lenders typically view it as less risky than unsecured loans (like credit cards or personal loans). This lower risk translates to lower interest rates for you. We're talking potentially single-digit interest rates, which can be a massive improvement if you're currently paying 15%, 20%, or even 25% on your other debts. A lower interest rate means more of your monthly payment goes towards the principal balance, helping you pay off your debt faster and saving you a significant amount of money over the life of the loan. Plus, with a lower interest rate, your minimum monthly payments will likely be much smaller, freeing up cash flow in your budget.

Flexible Access to Funds and Revolving Credit Line Benefits

Unlike a traditional debt consolidation loan that gives you a one-time lump sum, a HELOC offers flexibility. You can draw funds as needed during a 'draw period,' which typically lasts 5 to 10 years. This can be useful if you anticipate needing to pay off debts in stages or if you want to keep a portion of the credit line available for future emergencies (though using it for emergencies when you're trying to consolidate debt can be a slippery slope, so be careful!). You only pay interest on the amount you've actually borrowed, not the entire credit limit. This flexibility can be a double-edged sword, which we'll discuss later, but for some, it's a huge plus.

Potential Tax Deductibility of HELOC Interest

Here's another sweet perk: the interest you pay on a HELOC might be tax-deductible. Under current tax laws (always check with a tax professional for the most up-to-date information!), interest on home equity debt can be deductible if the funds are used to 'buy, build, or substantially improve' the home that secures the loan. While using it for debt consolidation doesn't directly fall into that category, if you also use a portion of the HELOC for home improvements, that portion of the interest could be deductible. This isn't a primary reason to get a HELOC for debt consolidation, but it's a nice bonus to be aware of if applicable to your situation.

Simplified Debt Management with One Monthly Payment

Imagine going from five or six different debt payments each month, all with different due dates, minimums, and interest rates, to just one single payment. Sounds pretty good, right? That's the beauty of debt consolidation with a HELOC. It streamlines your financial life, making it much easier to keep track of your obligations and avoid missing payments, which can hurt your credit score.

The Significant Disadvantages and Risks of HELOC Debt Consolidation

Okay, so a HELOC sounds pretty great so far, right? Lower interest, flexibility, potential tax benefits. But hold your horses! There are some serious downsides and risks you absolutely need to consider before you even think about going down this path. These aren't minor issues; they can have huge implications for your financial future.

Your Home is Collateral The Ultimate Risk of Foreclosure

This is the biggest, most critical disadvantage. When you take out a HELOC, your home serves as collateral. This means if you fail to make your payments, the lender has the legal right to foreclose on your home. You could lose your house. This is a far more severe consequence than defaulting on a credit card or personal loan, where the worst outcome is usually a damaged credit score and collections, not losing your roof over your head. This risk alone makes a HELOC a very serious financial commitment that demands careful consideration and a rock-solid repayment plan.

Variable Interest Rates and Payment Fluctuations

Most HELOCs come with variable interest rates. This means the interest rate isn't fixed; it can go up or down based on a benchmark index, usually the prime rate. While a low variable rate can be great when rates are low, it also means your monthly payments can increase if interest rates rise. This can throw a wrench in your budget, especially if you're already stretching to make ends meet. Imagine consolidating your debt at a 5% HELOC rate, only to see it jump to 8% or 10% a few years later. Your payments would increase, potentially making it harder to afford and increasing your risk of default.

The Temptation to Overspend and Accumulate New Debt

Remember that flexibility we talked about? It can be a double-edged sword. Because a HELOC is a revolving line of credit, it can be tempting to draw more money than you initially intended, or worse, to run up new debt on your old credit cards after you've paid them off with the HELOC. If you lack strong financial discipline, you could end up in a worse position than when you started – with a HELOC payment AND new credit card debt. This is a common pitfall, and it's crucial to have a clear plan and stick to it.

Closing Costs and Fees Associated with HELOCs

Just like with a traditional mortgage, HELOCs often come with various fees and closing costs. These can include application fees, appraisal fees, annual fees, and sometimes even transaction fees for each draw. While some lenders might offer HELOCs with no closing costs, they often make up for it with higher interest rates. These upfront costs can eat into the savings you hope to achieve through consolidation, so it's important to factor them into your overall calculation.

Long Repayment Periods and Extended Debt Horizon

HELOCs typically have two phases: a draw period (usually 5-10 years) where you can borrow and make interest-only payments, and a repayment period (usually 10-20 years) where you pay back both principal and interest. While the lower monthly payments can be appealing, the overall repayment period can be quite long, potentially extending your debt obligations for decades. If your goal is to become debt-free quickly, a HELOC might not be the fastest route, especially if you only make minimum payments during the draw period.

When a HELOC Might Be a Good Fit for Debt Consolidation

So, with all those pros and cons, when does a HELOC actually make sense for debt consolidation? It's not for everyone, but it can be a powerful tool under the right circumstances:

- You have significant home equity: You need enough equity to borrow a meaningful amount to pay off your high-interest debts.

- You have a stable income and excellent credit: Lenders will be more willing to offer you favorable rates and terms if you have a strong financial profile.

- You have a solid plan to repay the HELOC: This isn't a magic bullet. You need a realistic budget and a commitment to making consistent payments.

- You have high-interest, unsecured debt: If your current debts are costing you a fortune in interest, a HELOC's lower rate can offer substantial savings.

- You have strong financial discipline: You must be able to resist the temptation to draw more funds or run up new debt.

- You understand and accept the risk of using your home as collateral: This is non-negotiable. You must be comfortable with this level of risk.

When a HELOC is NOT a Good Idea for Debt Consolidation

Conversely, there are clear situations where a HELOC is absolutely the wrong choice:

- You have limited home equity: If you don't have much equity, you won't be able to borrow enough to make a difference, or you might not even qualify.

- Your income is unstable or you have poor credit: You might not qualify for a good rate, or you might struggle to make payments.

- You lack financial discipline: If you've struggled with overspending in the past, a HELOC could lead to even more debt.

- You're uncomfortable risking your home: If the thought of losing your home keeps you up at night, a HELOC is not for you.

- You're close to retirement: Taking on a long-term debt secured by your home late in life can be very risky.

- You're planning to sell your home soon: A HELOC can complicate the sale process.

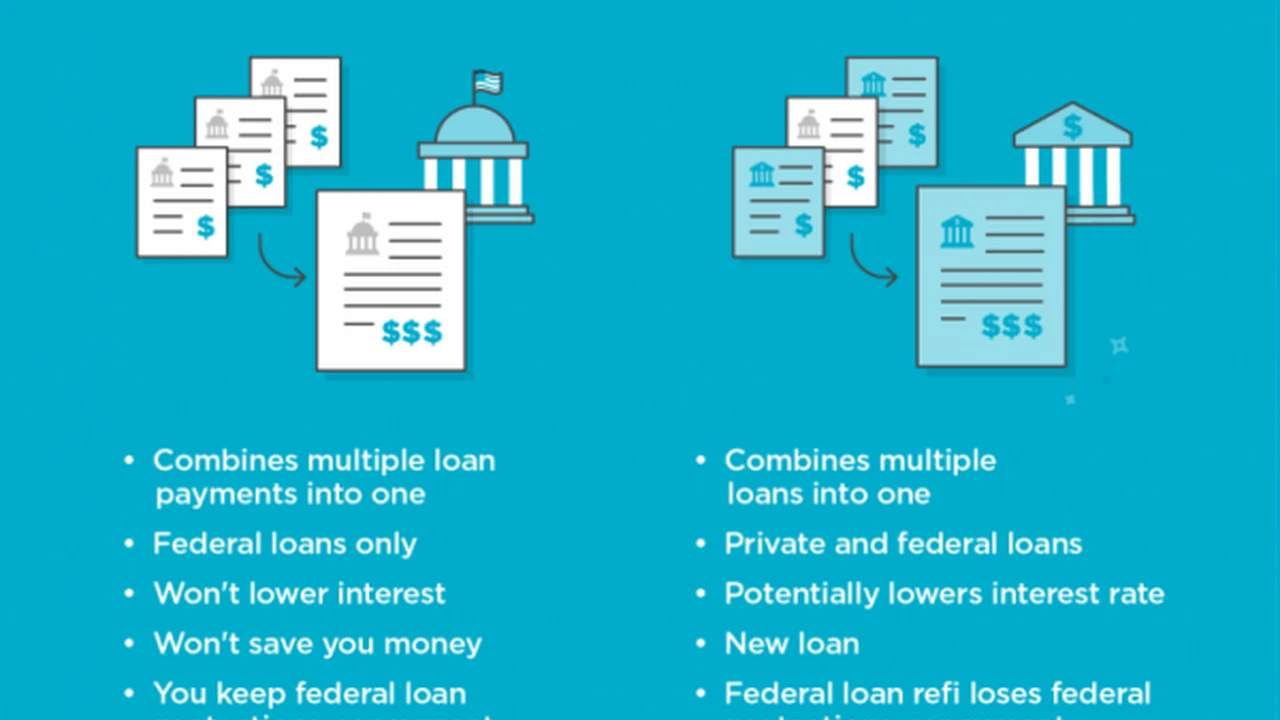

Comparing HELOCs with Other Debt Consolidation Options

It's crucial to see how a HELOC stacks up against other popular debt consolidation methods. This will help you make a truly informed decision.

HELOC vs Personal Loans for Debt Consolidation

Personal loans are unsecured, meaning they don't require collateral. This is a huge difference. If you default on a personal loan, you won't lose your home. Personal loans typically have fixed interest rates, so your payments remain predictable. However, their interest rates are usually higher than HELOCs, especially for those with less-than-perfect credit. The repayment terms are also generally shorter (3-7 years), which means higher monthly payments but a faster path to being debt-free. For someone who doesn't want to risk their home or prefers predictable payments, a personal loan might be a better fit, even with a slightly higher interest rate.

HELOC vs Balance Transfer Credit Cards for Debt Consolidation

Balance transfer credit cards offer an introductory 0% APR period, usually for 12-21 months. This can be fantastic for paying down debt quickly without incurring interest. However, you typically need excellent credit to qualify for the best offers, and there's usually a balance transfer fee (around 3-5% of the transferred amount). The biggest catch is that if you don't pay off the balance before the promotional period ends, the remaining balance will be subject to a much higher, often variable, interest rate. This option is best for those with excellent credit who can commit to paying off the transferred balance within the introductory period. It carries no risk to your home.

HELOC vs Cash-Out Refinance for Debt Consolidation

A cash-out refinance involves replacing your existing mortgage with a new, larger mortgage, and you receive the difference in cash. This cash can then be used to pay off other debts. Like a HELOC, it's secured by your home and typically offers very low, fixed interest rates. The main difference is that it's a new, single loan, not a revolving line of credit. This means you get a lump sum, and your entire mortgage term restarts, potentially extending your mortgage payments for another 30 years. It's a good option if you want a fixed rate and a lump sum, but it resets your mortgage clock and might involve higher closing costs than a HELOC.

Choosing a HELOC Lender and Understanding Product Details

If you've weighed the pros and cons and decided a HELOC might be right for you, the next step is to shop around for lenders. Don't just go with your current bank without checking other options. Here's what to look for and some examples of products (note: these are general examples, and specific terms will vary based on market conditions, your credit, and the lender):

Key Factors When Comparing HELOC Products

- Interest Rate (APR): Look for the lowest possible rate. Understand if it's variable or if there's an option for a fixed-rate draw.

- Draw Period and Repayment Period: How long can you access funds? How long do you have to pay it back?

- Fees: Application fees, annual fees, closing costs, inactivity fees, early closure fees. Get a full breakdown.

- Loan-to-Value (LTV) Ratio: This is the percentage of your home's equity the lender will allow you to borrow against. Most are 80-90%.

- Minimum Draw Amount: Some HELOCs require a minimum amount each time you draw funds.

- Payment Options: Can you make interest-only payments during the draw period? What are the minimum payment requirements?

- Customer Service and Reputation: Read reviews and choose a reputable lender.

Example HELOC Products and Scenarios (Illustrative, not specific recommendations)

Let's imagine a few scenarios and some hypothetical HELOC products that might fit:

Scenario 1: Excellent Credit, Significant Equity, Disciplined Borrower

You have a credit score above 760, 40% equity in your home, and a proven track record of managing debt responsibly. You want to consolidate $50,000 in credit card debt with an average APR of 22%.

- Hypothetical Product: 'Premier Equity Line' from a major bank (e.g., Chase, Bank of America, Wells Fargo)

- Interest Rate: Prime Rate + 0.50% (e.g., if Prime is 8.50%, your rate is 9.00% variable). Some might offer an introductory fixed rate for 6-12 months.

- Credit Limit: Up to 90% LTV.

- Fees: No annual fee, no closing costs if initial draw is above $10,000.

- Draw Period: 10 years, followed by a 20-year repayment period.

- Use Case: Ideal for consolidating high-interest debt, with the potential for significant interest savings. The borrower's discipline ensures they won't overspend.

Scenario 2: Good Credit, Moderate Equity, Need for Flexibility

Your credit score is around 700-740, you have 25% equity, and you want to consolidate $30,000 in various debts. You also anticipate needing a small amount for a home repair in the next year.

- Hypothetical Product: 'Flexible Home Equity Option' from a regional bank or credit union (e.g., Navy Federal Credit Union, local community bank)

- Interest Rate: Prime Rate + 1.00% (e.g., 9.50% variable). May have a cap on how high the rate can go.

- Credit Limit: Up to 85% LTV.

- Fees: Low annual fee ($50), some closing costs (e.g., $500-$1000) that can be rolled into the loan.

- Draw Period: 7 years, followed by a 15-year repayment period.

- Use Case: Good for consolidating debt and having a small buffer for planned expenses. The slightly higher rate reflects the moderate credit and equity.

Scenario 3: Fair Credit, Limited Equity, Higher Risk Tolerance

Your credit score is in the mid-600s, and you have 20% equity. You want to consolidate $20,000 in debt, but your options for unsecured loans are limited or very expensive.

- Hypothetical Product: 'Secured Debt Relief HELOC' from a specialized lender or smaller bank

- Interest Rate: Prime Rate + 2.50% (e.g., 11.00% variable). Likely to have a higher floor and ceiling for the rate.

- Credit Limit: Up to 80% LTV.

- Fees: Higher closing costs (e.g., 1-2% of the credit limit), potential annual fee.

- Draw Period: 5 years, followed by a 10-year repayment period.

- Use Case: This is a riskier option due to the higher interest rate and potentially higher fees. It's for borrowers who have exhausted other options and are willing to take on the risk of a HELOC to escape even higher-interest debt. Strong discipline is absolutely critical here.

Remember, these are just illustrative examples. Always get personalized quotes from multiple lenders and compare the APR, fees, terms, and conditions carefully. Don't be afraid to ask questions and negotiate!

Practical Steps for Applying for a HELOC for Debt Consolidation

If you've decided a HELOC is worth exploring, here's a general roadmap of what to expect:

- Assess Your Home Equity: Get a rough estimate of your home's current market value (e.g., through online tools like Zillow or by consulting a local real estate agent) and subtract your outstanding mortgage balance. This gives you your equity.

- Check Your Credit Score: Lenders will pull your credit report. A higher score generally means better rates. Get a free copy of your credit report from AnnualCreditReport.com.

- Gather Your Financial Documents: You'll need proof of income (pay stubs, tax returns), bank statements, details of your existing debts, and information about your home (property tax statements, mortgage statements).

- Shop Around for Lenders: Contact several banks, credit unions, and online lenders. Compare their rates, fees, LTV limits, and terms. Don't just look at the advertised rate; ask for a personalized quote.

- Pre-qualification (Optional but Recommended): Some lenders offer pre-qualification, which gives you an idea of what you might qualify for without a hard credit inquiry.

- Submit Your Application: Once you choose a lender, complete the full application. This will involve a hard credit pull.

- Home Appraisal: The lender will likely require an appraisal of your home to confirm its value.

- Underwriting and Approval: The lender will review all your documents and the appraisal. If approved, you'll receive a loan offer.

- Closing: You'll sign the necessary documents, and there will typically be a waiting period (often 3 business days) before funds are disbursed, as required by law for home equity products.

- Pay Off Your Debts: Once you have access to the HELOC funds, immediately use them to pay off your high-interest debts. Close those credit card accounts if you can, or at least cut up the cards to avoid future temptation.

- Create a Repayment Plan: Develop a strict budget and a clear plan for how you will repay your HELOC. Stick to it!

Managing Your Finances After HELOC Debt Consolidation

Getting a HELOC for debt consolidation is just the first step. The real work begins afterward. Here's how to ensure long-term success:

Strict Budgeting and Spending Habits

This is non-negotiable. You need to create and stick to a detailed budget that accounts for your new HELOC payment and all other expenses. Track every dollar in and out. Identify areas where you can cut back to accelerate your HELOC repayment. The goal is to live within your means and avoid accumulating new debt.

Avoid New Debt at All Costs

This is where many people stumble. After consolidating, it's easy to feel a sense of relief and then fall back into old spending habits. Resist the urge to use those newly freed-up credit cards. If possible, close the accounts or at least put the cards away in a safe place where they're not easily accessible. Your primary focus should be on paying down the HELOC.

Build an Emergency Fund

One of the reasons people often fall into debt is unexpected expenses. Once you've consolidated, prioritize building an emergency fund of 3-6 months' worth of living expenses. This fund acts as a buffer, so you don't have to rely on credit cards or your HELOC for unforeseen costs like car repairs or medical bills.

Monitor Your Credit Score Regularly

Keep an eye on your credit score. As you pay down your HELOC and avoid new debt, your score should improve. A better credit score opens doors to better financial products in the future. You can get free credit reports and scores from various services.

Consider Making Extra Payments

If your budget allows, make more than the minimum payment on your HELOC. Even a little extra each month can significantly reduce the total interest paid and shorten your repayment period, especially with a variable interest rate. This is a powerful way to take control of your debt.

Review Your Financial Plan Periodically

Life changes, and so should your financial plan. Review your budget and debt repayment strategy every few months or at least once a year. Adjust as needed based on changes in income, expenses, or interest rates. Staying proactive is key to long-term financial health.

Using a HELOC for debt consolidation can be a powerful strategy to simplify your finances, lower your interest rates, and accelerate your path to debt freedom. However, it comes with significant risks, primarily the risk of losing your home. It's a tool best suited for disciplined individuals with substantial home equity and a clear understanding of the commitment involved. Always weigh the advantages against the disadvantages, compare it with other consolidation options, and if you're unsure, consider consulting with a financial advisor to determine the best course of action for your unique financial situation. Your home is your most valuable asset, so treat any decision involving it with the utmost care and consideration.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)