Top 3 Debt Consolidation Loans for Fair Credit Scores

Explore the best three debt consolidation loans available for those with fair credit helping you secure better terms.

Explore the best three debt consolidation loans available for those with fair credit helping you secure better terms.

Top 3 Debt Consolidation Loans for Fair Credit Scores

Understanding Fair Credit and Debt Consolidation Loans

So, you've got a fair credit score, and you're looking to get your finances in order. That's a fantastic step! Many people find themselves in this position, and it's completely understandable. A fair credit score, typically ranging from 580 to 669 on the FICO scale, means you've likely had a few bumps in your financial journey. Maybe you missed a payment or two, carried high credit card balances, or haven't had a long enough credit history to build an excellent score. Whatever the reason, it doesn't mean you're out of options when it comes to debt consolidation. In fact, debt consolidation can be a powerful tool to help you improve your credit score over time by simplifying your payments and potentially lowering your interest rates.

Debt consolidation is essentially taking out a new loan to pay off multiple existing debts, like credit card balances, medical bills, or personal loans. The goal is to combine these into one single, more manageable monthly payment, often with a lower interest rate. This can make it easier to track your payments, reduce the total amount of interest you pay, and free up some cash flow. For someone with a fair credit score, finding the right debt consolidation loan is crucial. You might not qualify for the absolute lowest rates, but there are still excellent options out there that can significantly improve your financial situation.

Why Fair Credit Matters for Debt Consolidation Loan Approval

Your credit score is a snapshot of your financial reliability. Lenders use it to assess the risk of lending you money. A fair credit score tells them you're a moderate risk. This means they might offer you slightly higher interest rates than someone with excellent credit, or they might require a co-signer or collateral. However, many lenders specialize in working with borrowers across the credit spectrum, including those with fair credit. They understand that everyone deserves a chance to get their finances back on track.

When you apply for a debt consolidation loan, lenders will look at several factors beyond just your credit score. They'll consider your income, your debt-to-income ratio (how much debt you have compared to your income), your employment history, and any existing assets. Even with a fair credit score, a strong income and a stable job can significantly boost your chances of approval and help you secure better terms. It's all about presenting a complete picture of your financial health.

Our Top 3 Debt Consolidation Loan Picks for Fair Credit Scores

After extensive research and considering various factors like interest rates, fees, customer service, and accessibility for fair credit borrowers, we've narrowed down our top three recommendations. These lenders have a proven track record of helping individuals with fair credit achieve their debt consolidation goals.

1. Upgrade Personal Loans for Fair Credit Debt Consolidation

Overview: Upgrade is a popular online lender known for its accessible personal loans, even for those with less-than-perfect credit. They offer a streamlined application process and often provide quick funding, which can be a huge plus when you're eager to tackle your debt. Upgrade specifically caters to a wide range of credit scores, making them a strong contender for fair credit borrowers.

Key Features for Fair Credit Borrowers:

- Lower Credit Score Requirements: Upgrade typically accepts credit scores as low as 580, putting them squarely in the fair credit category.

- Secured Loan Options: For those with fair credit who might struggle to get approved for an unsecured loan or want a lower interest rate, Upgrade offers secured personal loans. You can use a vehicle as collateral, which can significantly improve your chances of approval and get you a more favorable rate.

- Direct Pay to Creditors: Upgrade can directly pay off your existing creditors, simplifying the consolidation process and ensuring your old debts are settled efficiently. This feature is incredibly helpful for ensuring the funds go exactly where they're intended.

- Flexible Loan Amounts and Terms: They offer a range of loan amounts, typically from $1,000 to $50,000, with repayment terms often between 2 to 7 years. This flexibility allows you to tailor the loan to your specific debt amount and budget.

- No Prepayment Penalties: You can pay off your loan early without incurring any extra fees, which is great if you find yourself in a better financial position sooner than expected.

Typical Use Cases: Upgrade is excellent for consolidating high-interest credit card debt, medical bills, or other personal loans. Their secured loan option is particularly useful if you have a car with equity and want to leverage it for better loan terms. It's also a good choice for those who prefer an entirely online application and management experience.

Potential Drawbacks: While accessible, interest rates for fair credit borrowers can still be on the higher side compared to those with excellent credit. They also charge an origination fee, which is deducted from your loan proceeds, so factor that into your total cost.

Estimated Pricing (Illustrative, actual rates vary):

- APR Range: Typically from 8% to 36% (fair credit borrowers will likely be in the higher end of this range, especially for unsecured loans).

- Origination Fee: 1.85% to 9.99% of the loan amount.

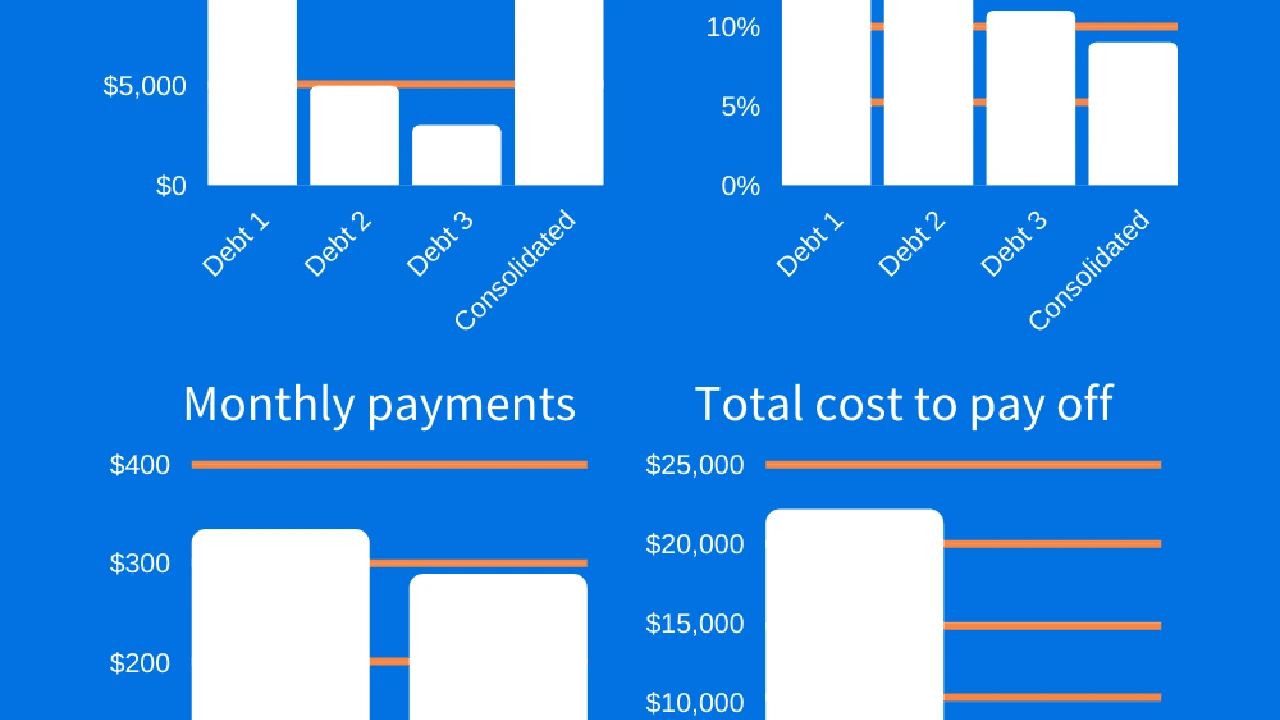

- Example Scenario: A $10,000 loan with a 25% APR and a 5% origination fee over 36 months would result in an origination fee of $500, and monthly payments around $398. Total interest paid would be approximately $4,328.

2. Avant Personal Loans for Debt Consolidation with Fair Credit

Overview: Avant is another strong contender for fair credit borrowers, specializing in personal loans for individuals with credit scores in the fair to good range. They pride themselves on a quick and straightforward application process, often providing a decision within minutes and funding as soon as the next business day. Avant understands the needs of borrowers who might not have perfect credit but are committed to improving their financial standing.

Key Features for Fair Credit Borrowers:

- Accessible Credit Requirements: Avant generally accepts credit scores starting from 580, making them a viable option for many with fair credit.

- Fast Funding: If approved, funds can often be deposited into your bank account as early as the next business day, which is beneficial if you need to consolidate debts quickly.

- Fixed Interest Rates: All Avant loans come with fixed interest rates, meaning your monthly payment will remain the same throughout the loan term, providing predictability and ease of budgeting.

- Manageable Loan Amounts: They offer loans typically ranging from $2,000 to $35,000, which is suitable for consolidating a significant amount of consumer debt.

- Flexible Repayment Terms: Repayment periods usually range from 24 to 60 months, allowing you to choose a term that fits your budget.

Typical Use Cases: Avant is ideal for consolidating credit card debt, personal loans, or other unsecured debts. It's a good fit for those who value speed and a clear, fixed repayment schedule. If you have a few different debts that you want to roll into one predictable payment, Avant can be a great solution.

Potential Drawbacks: Similar to Upgrade, Avant's interest rates for fair credit borrowers can be higher than what someone with excellent credit would receive. They also charge an administrative fee (origination fee) that can be up to 4.75% of the loan amount.

Estimated Pricing (Illustrative, actual rates vary):

- APR Range: Typically from 9.95% to 35.99%.

- Administrative Fee: Up to 4.75% of the loan amount.

- Example Scenario: A $8,000 loan with a 28% APR and a 4% administrative fee over 48 months would result in an administrative fee of $320, and monthly payments around $280. Total interest paid would be approximately $5,120.

3. LendingClub Personal Loans for Debt Consolidation

Overview: LendingClub operates as a peer-to-peer lending platform, which means your loan is funded by individual investors rather than a traditional bank. This model can sometimes offer more flexibility for borrowers with fair credit. LendingClub has been a pioneer in the online lending space and has helped millions consolidate debt.

Key Features for Fair Credit Borrowers:

- Lower Minimum Credit Score: LendingClub typically requires a minimum FICO score of 600, making it accessible for many fair credit individuals.

- Direct Pay Option: Like Upgrade, LendingClub can send funds directly to your creditors, streamlining the debt consolidation process and ensuring your old accounts are paid off.

- Joint Applications: You can apply for a joint loan with a co-borrower, which can significantly improve your chances of approval and potentially secure a lower interest rate if the co-borrower has better credit. This is a huge advantage for fair credit borrowers.

- Fixed Rates and Terms: LendingClub offers fixed interest rates and terms, usually 36 or 60 months, providing predictable monthly payments.

- Financial Education Resources: They offer various resources to help borrowers understand their finances better, which can be valuable for long-term financial health.

Typical Use Cases: LendingClub is excellent for consolidating credit card debt, personal loans, and other unsecured debts. It's particularly beneficial if you have a co-borrower with good credit who can help you secure better terms. It's also a good option if you appreciate the transparency of a peer-to-peer model.

Potential Drawbacks: LendingClub charges an origination fee, which can range from 3% to 6% of the loan amount. The funding process can sometimes take a bit longer than direct online lenders, as it depends on investors funding your loan. Interest rates for fair credit borrowers will still be higher than for those with excellent credit.

Estimated Pricing (Illustrative, actual rates vary):

- APR Range: Typically from 8.05% to 35.89%.

- Origination Fee: 3% to 6% of the loan amount.

- Example Scenario: A $12,000 loan with a 22% APR and a 4% origination fee over 60 months would result in an origination fee of $480, and monthly payments around $335. Total interest paid would be approximately $7,620.

Comparing the Best Debt Consolidation Loans for Fair Credit

When you're looking at these options, it's not just about the lowest advertised rate. You need to consider the full picture. Here's a quick comparison table to help you visualize the differences:

| Feature | Upgrade | Avant | LendingClub |

|---|---|---|---|

| Minimum Credit Score | 580 | 580 | 600 |

| Loan Amounts | $1,000 - $50,000 | $2,000 - $35,000 | $1,000 - $40,000 |

| APR Range (Illustrative) | 8% - 36% | 9.95% - 35.99% | 8.05% - 35.89% |

| Origination/Admin Fee | 1.85% - 9.99% | Up to 4.75% | 3% - 6% |

| Funding Speed | 1-4 business days | Next business day | Up to 7 business days |

| Direct Pay to Creditors | Yes | No | Yes |

| Secured Loan Option | Yes (vehicle) | No | No |

| Joint Application | No | No | Yes |

As you can see, each lender has its unique strengths. Upgrade offers secured loan options, which can be a game-changer for some. Avant is known for its speed, and LendingClub allows for joint applications. Your best choice will depend on your specific needs, the amount you need to borrow, and whether you have a co-borrower or collateral available.

Strategies for Securing the Best Debt Consolidation Loan with Fair Credit

Even with a fair credit score, there are things you can do to improve your chances of approval and get the most favorable terms possible. Think of it as optimizing your application!

Improving Your Credit Score Before Applying for Debt Consolidation

Even a small bump in your credit score can make a difference. Before you apply, try to:

- Pay down small balances: Reducing your credit utilization (the amount of credit you're using compared to your total available credit) can quickly boost your score.

- Make all payments on time: Payment history is the biggest factor in your credit score. Even one late payment can hurt.

- Check your credit report for errors: Mistakes happen! Dispute any inaccuracies you find on your credit report with all three major credit bureaus (Experian, Equifax, TransUnion).

- Avoid new credit applications: Each new application can cause a small dip in your score.

Considering a Co-signer for Better Loan Terms

If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can significantly improve your chances of approval and help you secure a much lower interest rate. A co-signer essentially guarantees the loan, reducing the risk for the lender. However, remember that a co-signer is equally responsible for the debt, so it's a serious commitment for both parties.

Exploring Secured Debt Consolidation Loan Options

As mentioned with Upgrade, some lenders offer secured personal loans where you use an asset, like a car or savings account, as collateral. This reduces the lender's risk, making them more willing to approve your loan and offer a lower interest rate. Just be aware that if you fail to repay the loan, you could lose the asset you put up as collateral.

Gathering All Necessary Documentation for a Smooth Application

Be prepared! Having all your documents ready before you apply can speed up the process. This typically includes:

- Proof of identity (driver's license, passport)

- Proof of address (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Details of the debts you want to consolidate (account numbers, current balances, interest rates)

Understanding the Total Cost of the Debt Consolidation Loan

Don't just look at the monthly payment. Always consider the Annual Percentage Rate (APR), which includes the interest rate and any fees (like origination fees). A lower monthly payment over a longer term might seem appealing, but it could mean you pay more in total interest over the life of the loan. Use online calculators to compare the total cost of different loan offers.

The Application Process for Debt Consolidation Loans

Applying for a debt consolidation loan, especially with online lenders, is usually a straightforward process. Here's a general idea of what to expect:

Pre-qualification and Soft Credit Checks

Many lenders, including the ones we've highlighted, offer a pre-qualification process. This allows you to see potential loan offers and interest rates without impacting your credit score. They perform a 'soft' credit inquiry, which doesn't show up on your credit report as a hard inquiry. This is a great way to shop around and compare offers from multiple lenders before committing to a full application.

Submitting Your Full Application and Documentation

Once you've pre-qualified and chosen a lender, you'll proceed with the full application. This involves providing more detailed personal and financial information and submitting the required documents. At this stage, the lender will typically perform a 'hard' credit inquiry, which will temporarily ding your credit score by a few points. This is normal and expected.

Loan Approval and Funding Disbursement

If your application is approved, you'll receive a loan offer outlining the terms, interest rate, and repayment schedule. Read this carefully! Once you accept the offer, the funds will be disbursed. As mentioned, some lenders can send the money directly to your creditors, while others will deposit it into your bank account for you to pay off your debts. Make sure you understand how the funds will be distributed and follow through to ensure all your old debts are paid off.

Managing Your Finances After Debt Consolidation

Getting a debt consolidation loan is a huge step, but it's just the beginning. The real work starts after you've consolidated your debts. This is your chance to build healthier financial habits and ensure you don't fall back into debt.

Creating a Realistic Budget and Sticking to It

Now that you have one predictable monthly payment, it's easier to budget. Create a detailed budget that accounts for your new loan payment, all your other expenses, and allocates funds for savings. Track your spending diligently to ensure you're staying within your budget. There are many free budgeting apps and tools available to help you with this.

Avoiding New Debt and Building an Emergency Fund

The primary goal of debt consolidation is to get out of debt, not to create room for more. Be disciplined about not taking on new credit card debt or unnecessary loans. Instead, focus on building an emergency fund. Aim for at least 3-6 months' worth of living expenses. This fund will act as a buffer against unexpected costs, preventing you from relying on credit cards again.

Monitoring Your Credit Score for Improvement

As you consistently make on-time payments on your consolidated loan, your credit score should gradually improve. Keep an eye on it! You can get free credit reports annually from AnnualCreditReport.com and many credit card companies and banks offer free credit score monitoring. Seeing your score rise can be a great motivator and a sign that your hard work is paying off.

Considering Refinancing in the Future

Once your credit score has improved significantly, you might be able to refinance your debt consolidation loan for an even lower interest rate. This could save you even more money over the life of the loan. Keep this in mind as a long-term goal once you've established a solid payment history.

Debt consolidation for fair credit borrowers is absolutely achievable. By understanding your options, preparing your application, and committing to responsible financial habits afterward, you can successfully navigate your way to a more stable and debt-free future. It takes effort, but the peace of mind and financial freedom are well worth it.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)